Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

Mini budget:

reality catches up with hope

Our new Finance Minister, Tito Mboweni, certainly delivered his maiden Medium-Term Budget Policy Statement (MTBPS) in a statesman-like fashion last week. He was honest to a fault, not beating around the bush in setting out the fiscal predicament of our government. The macro numbers – in particular fiscal slippage and our country’s debt burden – remain of grave concern, however, and reflect the reality of an economy stuck in a low-growth trap.

The macro-economic backdrop against which Minister Mboweni had to present his mini budget to Parliament didn’t give him much room to manoeuvre. In the prevailing economic conditions, revenue was sure to be under pressure. Our new Finance Minister also inherited an alarmingly high budget deficit, certainly in international terms. So there wasn’t too much he could do under the circumstances except rearrange the deck chairs.

Most analysts didn’t anticipate too much fiscal slippage, which simply refers to the difference between the expected and the actual deficit. There was also some expectation that further detail on President Cyril Ramaphosa’s R50 billion infrastructure programme might be revealed, with funds being channelled into areas that could create capacity to grow the economy.

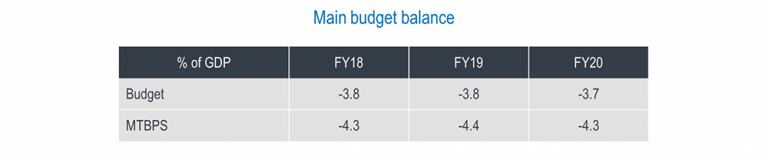

The mini budget disappointed in three main areas:

There are somewhat extenuating circumstances for this state of affairs – in the form of the VAT refund liability to the tune of R11 billion, which Minister Mboweni has committed to repaying to the business sector. But in the end, it remains a numbers game and both the bond and currency markets reacted negatively after the mini budget was tabled.

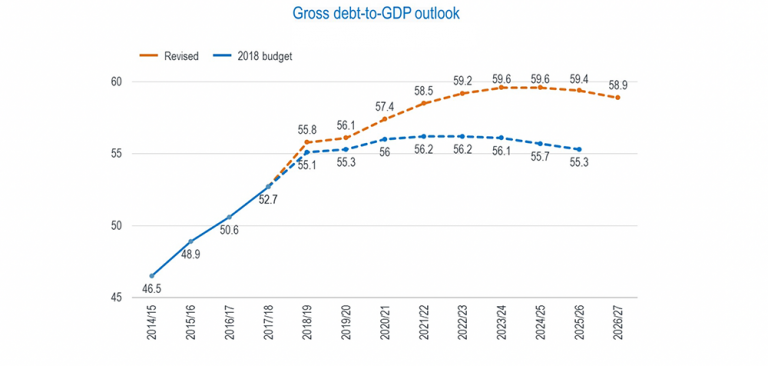

As this graph shows, the prediction in February was that our debt-to-GDP ratio would flatten out at around 56.2% by 2022 and then roll over towards 55.3% heading into 2025. In Minister Mboweni’s new forecast, gross national debt is now projected to peak at 59.6% – and only in 2023 – before slowly edging off. While he is to be commended for his honesty in presenting what’s probably a more realistic scenario than his predecessors, the new numbers aren’t going to please the rating agencies waiting in the wings.

We also noted that our Finance Minister didn’t provide much detail around how government intends to tackle financial discipline within state-owned enterprises (SOEs). A fair amount has been allocated to SAA (R5 billion), SA Express (R1.2 billion), the SA Post Office (R2.9 billion) and SANRAL (R5.8 billion), with promises that this will be the last funding of SAA. We have, of course, heard this before.

The aspects of the mini budget that we did like, include:

What does all this mean for investors? The financial markets weren’t too positive about the mini budget, as evidenced by the negative reaction of our currency. The markets are clearly concerned about the potential response of rating agencies to especially the higher gross debt levels. In our view, there’s now an increased likelihood that Moody’s – the sole agency that hasn’t yet downgraded South Africa’s sovereign debt to sub-investment grade – may respond by doing so, or at the least changing the outlook to negative.

Bond yields also came under pressure in the wake of Minister Mboweni’s speech. As a result of the increased deficit, Treasury will now need to fund an additional R175 billion in terms of bond issuance, which will of course push down bond prices.

The mini budget is in the main good news for equity markets, however. The corporate sector will welcome the envisaged overdue VAT refunds. The VAT exemptions on certain items from April next year should also provide a boost to the food and other producers concerned.

Favourable for retail equities is the fact that Treasury hasn’t budgeted for increased taxes. And the proposed spending reallocation is sure to benefit certain segments of the private sector, such as the construction industry.

In a nutshell, we believe that the disappointments in the mini budget are fairly evenly balanced out by the positives, given the weak macro-economic backdrop. We remain very concerned about South Africa’s distressing gross national debt-to-GDP ratio, however. As always, we’ll structure portfolios to protect our clients’ investments against risks associated with this and other macro-economic and fiscal challenges.

We provide daily reporting of trades, monthly portfolio evaluations and annual tax reports to clients.

Riaan Gerber has spent 16 years in Investment Management.

Have a question for Riaan?