Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

PLATINUM SECTOR:

PROSPECTS STILL POSITIVE

Like most industries, the platinum group metals (PGM) sector has been severely impacted by the ongoing COVID-19 pandemic. Platinum, palladium and rhodium are used mainly in auto catalysts, and global new car sales are estimated to decline by 20% this year. We remain upbeat about the medium-term prospects for the sector, however, as supply growth remains muted and tighter emissions standards drive increased loadings per vehicle. Our preferred pick is Northam, which, unlike its peers, is ramping up new low-cost supply of these metals at one of its mines.

Read more below or listen to Christiaan's views here:

PGMs refer to the six precious metals clustered together in the centre of the periodic table of elements: platinum, palladium, rhodium, osmium, iridium and ruthenium. For miners of these metals, the focus is mainly on the first three (3E), as these are the most abundant and/or the most useful.

The amount of each metal mined varies by geography and reef type. South African reefs generally have a high platinum content (typically more than 50% of the 3E metals, except for the northern limb of the Bushveld Complex in Limpopo, where palladium is more dominant).

South Africa produces most of the world’s platinum and rhodium – around 70% and 80% respectively of all new mined supply. Russia mines the most palladium globally at 40%, followed by South Africa in close second.

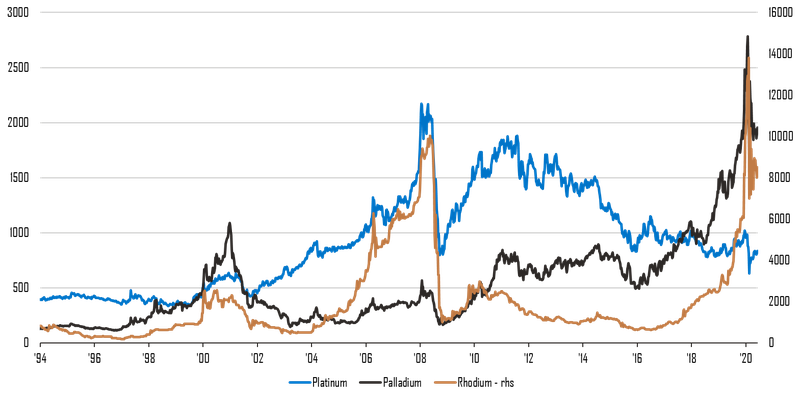

The prices of these three metals are currently quite different. At the time of writing, platinum was trading at about US$840/oz, palladium at US$1 950/oz and rhodium at over US$8 500/oz. As can be seen on the graph below, this hasn’t always been the case:

PGM prices: US$/oz

Source: IGraph

Why this significant divergence in prices for metals seemingly so similar in nature? The answer lies in their biggest source of demand: auto catalysts (nearly 65% of all 3E demand). Installed in car exhaust systems, these metals have the important role of converting harmful emissions into less hazardous ones.

The ratio of the three metals used depends on many factors, including the type of car engine (petrol or diesel), the position of the catalyst (close to the engine or underneath the car), the type of emissions (carbon monoxide, nitrogen oxide or sulphur oxide) and the security of metal supply.

Petrol engines – often referred to as gasoline engines – have traditionally used more palladium due to its ability to perform better at higher temperatures close to the engine. Diesel engines tend to use more platinum due to their historically high sulphur oxide content (which platinum breaks down better than palladium). Palladium has also been favoured over platinum in the past since the latter has a large exposure to South Africa compared to the more global supply diversification of palladium.

After the 2015 Volkswagen diesel scandal (Volkswagen was found to have inserted a cheat device to make emissions look lower in the laboratory versus on the road), sentiment for the use of the fuel in passenger vehicles decreased dramatically. Gasoline vehicles gained significant market share over diesel, most notably in Western Europe where the share of new diesel passenger car sales fell from over 50% in 2015 to a low of 30% in 2019.

The scandal also led to increased scrutiny of automakers, more stringent emission and real-driving emission requirements, and an increased focus on nitrogen oxide emissions. Meeting these new requirements meant increased amounts of 3E metals used per vehicle. China is the latest country to implement new standards, raising the average palladium required per vehicle from around 3g in 2018 to 5g by 2021.

The combination of lower diesel sales and increased emissions standards have resulted in soaring palladium prices as deficits have increased, while platinum prices have remained depressed due to a still-large surplus of metals. We have in the past argued that over time, the amount of platinum used in gasoline engines will increase at the expense of palladium, leading to prices converging.

Substitution hasn’t happened to the extent we’d anticipated, for a number of reasons. First, as mentioned above, palladium performs better in gasoline engines, making switching more difficult (this was easier in the past when emissions requirements were less stringent). Second, the catalyst is a small but vital component in the car and in the near term the focus is on compliance, with fines for not meeting the emissions targets much higher than the increased costs of the metal.

Despite the lack of large-scale substitution, it remains a likely scenario in some form or another over the next few years. Chemicals company BASF has already announced a new three-way catalyst using more platinum in gasoline vehicles, and there are signs of partial substitution of palladium in diesel cars. We remain of the view that the prices of palladium and platinum are likely to converge over the next two to five years, albeit at a slower pace than initially anticipated.

The performance of this little-known precious metal has surprised many analysts (including myself). It has a profound impact on the profits of PGM miners. With a total market of just more than 1 million ounces used per annum (palladium: 11 million ounces; platinum: around 8 million ounces), it plays a vital role in the three-way catalyst for reducing nitrogen oxide emissions. However, it’s much more efficient at doing so than either palladium or platinum (according to some estimates, around 4g of palladium is needed for every 1g of rhodium for the same performance).

The increased focus on nitrogen oxide after the diesel scandal played right into the hands of rhodium, but this is only half the story. At the same time, the supply side is very constrained. Rhodium is always mined as a small by-product to platinum and palladium (typically less than 10% of the mix) and is concentrated in deep-level mines in South Africa, where shafts are being closed over the next decade. It’s been estimated that supply will decline by on average 2% per annum over the next 10 years with large deficits anticipated, which is likely to keep prices elevated.

COVID-19 has had profound consequences in all our lives – one of which is the need and ability to buy new cars. Although nothing is certain at this stage, some estimates indicate that global new vehicle sales may decline by about 20% in 2020, which will have a significant impact on PGM demand for use in auto catalysts. However, this impact will at least be partly offset by still-increasing loadings per vehicle, as argued above.

The pandemic has also impacted the supply of metals. Lockdowns have forced most South African producers to temporarily close their mines, followed by a slow ramp-up with most producers still operating below normal capacity. South African supply has been forecast to contract by 20-30% in 2020, which will further help alleviate the negative impact of vehicle sales on prices.

Looking beyond 2020, lower vehicle sales than anticipated over the next few years will reduce demand for PGMs. However, the medium-term supply outlook will also have an impact – several large projects in South Africa are now in doubt, which will keep mined supply growth muted.

Towards the end of this decade, electric vehicles will pose a significant threat to PGM demand, as they don’t need these metals. But even on positive estimates, large-scale adoption of electric vehicles will take time, with hybrid electric vehicles (which still require a catalyst) remaining a large part of the mix. In the meantime, vehicle manufacturers need to comply with ever-more stringent emissions standards, which supports PGM demand.

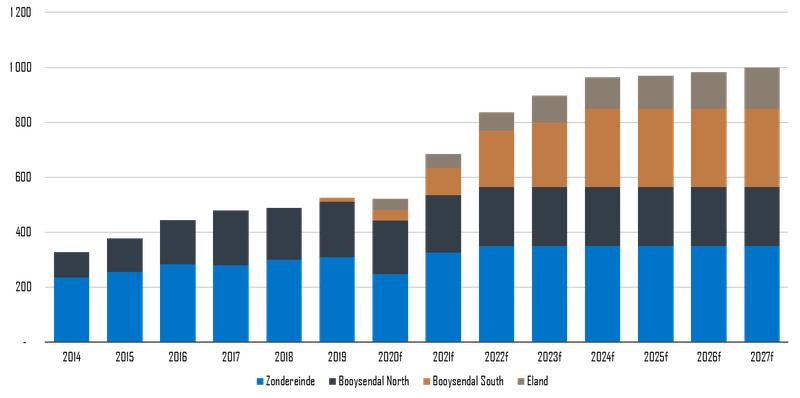

Our preferred pick in the PGM industry is Northam, which, unlike many of its peers, is ramping up new low-cost supply at the Booysendal South mine on the eastern limb of the Bushveld Complex. The company aims to produce around 1 million ounces of 4E metals (platinum, palladium, rhodium and gold) by 2027, up from around 0.57 million ounces in 2019 (see graph below).

In addition, the company reached its cash flow inflection point in December 2019, and is likely to generate healthy cash flows over the next few years as capital expenditure declines – which will mean good returns to shareholders.

Northam 4E PGM production (1 000 ounces)

Sources: company reports, SPW estimates

Investing in Northam is in our view also the best way to benefit from the highly positive outlook for rhodium, which makes up around 9% of the company’s 3E mix (compared to about 6% for Impala and Anglo American Platinum).

Overall, we believe 3E spot prices are too high at the moment (palladium and rhodium are too high, whereas platinum is too low). However, in our view, Northam’s current share price more than discounts for this fact. Moreover, the weaker currency provides a pleasant tailwind for South African miners with metals priced in dollars.

Using your equity portfolio to secure credit allows you fast access to capital.

Looking for a customised wealth plan? Leave your details and we’ll be in touch.