Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

SHOULD YOU GO FOR GOLD

IN YOUR PORTFOLIO?

Views on whether to include gold in an investment portfolio tend to be highly polarised – investors seem to either love it or fail to see the investment merits of the precious yellow metal. In our view, owning gold can be highly lucrative in an equity portfolio context – in times of crisis, it can provide valuable currency when other shares are cheap.

Gold tends to do well in an environment in which other risky assets struggle, but it performs poorly in times of economic expansion and increased risk appetite. One typically wants to own it when you expect real interest rates to decline (when you think central banks will start cutting interest rates or inflation will rise significantly while global growth slows – the so-called stagflation seen in the 1970s). Conversely, you need to be wary of gold investments when you expect interest rates to increase while inflation remains under control – this is typically when gold’s outlook relative to other asset classes doesn’t look too promising.

If you’re going for gold in your portfolio, the question arises as to which of gold shares or physical gold is the better choice. As is to be expected, gold equities have a strong correlation with gold prices (over the past decade, Goldfields and AngloGold Ashanti have shown a correlation coefficient of >0.7 to the rand gold price) and should therefore do well when gold prices rise. So as a starting point, the merits of gold shares are similar to those of physical gold – they tend to do well in an environment in which other risky assets perform poorly.

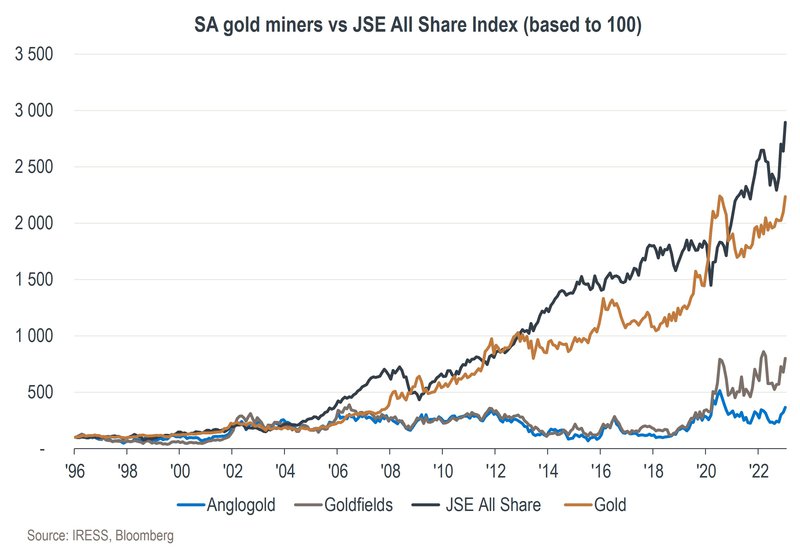

However, over the past few decades, gold shares have significantly underperformed both physical gold and the JSE All Share Index (ALSI) on a cumulative basis. From 1996, assuming dividends were reinvested, the ALSI returned 13% and the rand gold price 12% per annum, while Goldfields and AngloGold returned just 8% and 5% respectively. As can be seen on the chart below, R10 000 invested in 1996 in the ALSI would have yielded R289 500 today, compared to R223 500 for physical gold, R80 100 for Goldfields and R36 600 for AngloGold.

Gold company management teams globally have, on average, not been good allocators of capital. South African listed shares have also been faced with ageing and ever-deepening local mines, leading to company profits largely being spent on diversifying offshore while paying very low cash returns to shareholders. This has therefore not been an investment you wanted to own through the cycle – if you managed to make money from gold shares you needed to have traded them very well, as illustrated on the chart.

What is clear, however, is that there are certain times (for example, in 2008/09 and 2019/20) when owning gold equities can be very lucrative in an equity portfolio context. As we’ve mentioned, like physical gold, gold equities tend to perform well during a crisis when other shares don’t, providing valuable currency at a time when other shares are cheap.

After not owning gold shares for more than a decade, we decided to initiate a position in mid-2022, as we felt the macro backdrop presented several scenarios in which gold and gold shares could potentially do very well. The major risks were an inflation spiral where the US Federal Reserve (the Fed) did not have the ability or willingness to bring inflation under control as the economy weakened, or a large escalation in geopolitical tensions. In addition, we believed that the price of gold as insurance was at that stage not excessive – it was priced in line with the expectation for forward-looking real interest rates, and South African gold equities were trading on single-digit multiples.

Our preference was, and still is, for AngloGold Ashanti. Its large JSE-listed peer, Goldfields, had performed much better operationally over the preceding three years – it outperformed AngloGold by more than 100%. The latter had also been experiencing a leadership vacuum but found a credible CEO in the Colombian Alberto Calderon, with a clear strategy to improve the performance of the company’s mines. We were therefore of the view that there was ample room to catch up to Goldfields, off a low base.

AngloGold’s performance since then has surprised to the upside. At the time of writing, the company has rallied by more than 50% compared to the market’s 20% and rand gold prices’ 12%. This has led us to take profits, as we feel the cost of owning gold shares (insurance) has increased too much. In addition, with inflation cooling across the globe, the likelihood of stagflation (the real bull case for owning gold and gold shares) appears to have declined quite significantly.

Despite taking profits, we do, however, maintain a small weight in AngloGold, as there are still a few macro scenarios that could lead to an outcome where gold does even better. Most notably, we could yet see an escalation in geopolitical tensions or a severe global recession, which would force the Fed to change course and to start cutting interest rates. In these scenarios, we still see meaningful upside in the gold price and in gold shares.

Your wealth plan is designed with you in mind. Your financial reality, aspirations and risk profile.

Looking for a customised wealth plan? Leave your details and we’ll be in touch.