Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

AVDP now in

full swing

On 30 September this year, National Treasury issued a statement noting that the additional voluntary disclosure programme (AVDP – previously referred to as the special voluntary disclosure programme) would come into operation on 1 October, even though the applicable tax legislation had not yet been finalised.

The AVDP is aimed at providing South African residents with undisclosed foreign assets and income a final chance to regularise their tax affairs.

The Rates and Monetary Amounts and Amendment of Revenue Laws Bill (the Bill) containing the relevant AVDP legislation was finally tabled on 26 October when Finance Minister Pravin Gordhan delivered his Medium Term Budget Policy Statement. Although it has yet to become law, all indications are that the Bill will be enacted in its current form.

Here’s what you need to know about the tax relief measures contained in the Bill:

The above-mentioned new provision added to the Bill is to be welcomed, as it provides clarity regarding future capital gains tax liabilities arising from assets disclosed in terms of the AVDP. (This will now only be limited to gains made since 28 February 2015 for individuals, and for companies, since the last day of assessment ending on or before 28 February 2015.)

The legislation unfortunately provides no clear direction on when the AVDP or when the normal statutory voluntary disclosure programme (VDP) should be used – this will unfortunately have to be determined on a case-by-case basis.

Taxpayers who hold undeclared foreign assets and who are considering making use of the AVDP should obtain the following information and substantiating documentation:

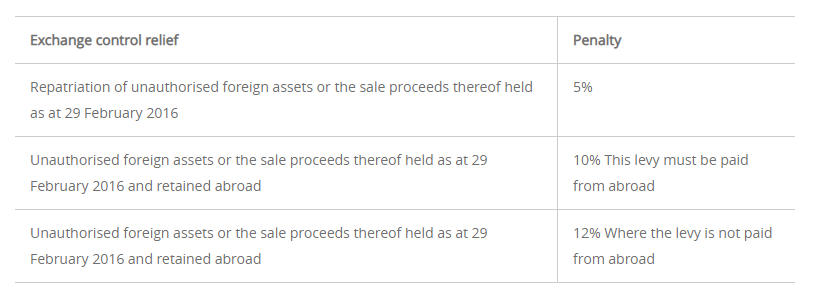

There have been no changes to exchange control measures. It seems relatively straightforward – the market value of assets in contravention of the Exchange Control Regulations as at 29 February 2016 must be disclosed.

The formation and registration of trusts, and the provision of independent trusteeships – both local and offshore.

The creation of BEE, charitable, special and Shariah trusts compliant with regulatory and legislative requirements.

The administration of deceased estates in South Africa and abroad.

Advice on complex structures, asset restructuring and bequests in foreign jurisdictions.

Advice on emigration and immigration, foreign earnings and the application of any double taxation agreements.

Updating trust deeds to ensure they’re in line with the latest changes in the trust environment.

Updating and/or drafting of wills dealing with South African and/or foreign assets.

Advice on the establishment and management of charitable organisations, their tax status and tax deductible donations.

Advice on the potential tax consequences and reporting obligations if you hold a US passport or green card, or if you have children living in the US.

Guidance on the financial implications of life-changing events, such as getting married, divorce or the birth of a child.

Documentary evidence to be supplied for the exchange control AVDP:

The indicative maximum ‘costs’ of the combined AVDP (tax and exchange control) would therefore be as follows:

As mentioned above, it is unlikely that the Bill will not be enacted in its current form, so taxpayers who want to make use of the AVDP are encouraged to obtain the required information as soon as possible to ensure they have enough time to submit their application before the window period ends on 30 June 2017.

If you have undisclosed assets we recommend that you contact a Sanlam Private Wealth Fiduciary and Tax specialist for professional advice and to assist you with the application process.

The formation and registration of trusts, and the provision of independent trusteeships – both local and offshore.

The creation of BEE, charitable, special and Shariah trusts compliant with regulatory and legislative requirements.

The administration of deceased estates in South Africa and abroad.

Advice on complex structures, asset restructuring and bequests in foreign jurisdictions.

Advice on emigration and immigration, foreign earnings and the application of any double taxation agreements.

Updating trust deeds to ensure they’re in line with the latest changes in the trust environment.

Updating and/or drafting of wills dealing with South African and/or foreign assets.

Advice on the establishment and management of charitable organisations, their tax status and tax deductible donations.

Advice on the potential tax consequences and reporting obligations if you hold a US passport or green card, or if you have children living in the US.

Guidance on the financial implications of life-changing events, such as getting married, divorce or the birth of a child.

Expert advice is crucial in dealing with cross-border estate and tax planning.

Stanley Broun has spent 13 years in Fiduciary And Tax.

Have a question for Stanley?