Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

Estate duty:

what you need to know

Former Finance Minister Malusi Gigaba announced in his February Budget Speech that from 1 March this year, estate duty would be increased from 20% to 25% on the ‘dutiable value’ of estates over R30 million. For all other estates in excess of R3.5 million up to R30 million, it remains at 20%. But what exactly is this ‘dutiable value’, and what’s included when the amount you need to pay is determined? Here’s what you need to know.

Estate duty in South Africa is charged on the ‘dutiable estate’ of a deceased individual – in other words, all property after allowable deductions, which include debts, funeral and death-bed expenses, administration costs, property accruing to a surviving spouse, and the first R3.5 million of the value of the property. It’s levied on the property of deceased persons ordinarily resident in South Africa, as well as on the South African property of persons who don’t ordinarily live here.

In terms of Section 3(2) of the Estate Duty Act No 45 of 1955 (the Act), foreign property is – for the purposes of South African estate duty – included as property in the dutiable estate of a person who ordinarily lives in this country.

In terms of Section 4A of the Act, a deduction of R3.5 million is allowed when determining the amount of estate duty to be paid. Deductions are also allowed for liabilities, bequests made to qualifying public benefit organisations, and property accruing to surviving spouses – either in terms of a will or by intestate succession.

In respect of the estate of a person dying on or after 1 January 2009, all benefits – including lump-sum benefits, payable from South African pension, provident and/or retirement annuity funds – are not deemed as ‘property’, and therefore not subject to estate duty.

In terms of Section 3(3)(a) of the Act, the proceeds of a life insurance policy are seen as property in the estate of a deceased person, except if:

The life insurance policies referred to above include policies where a spouse or child are nominated beneficiaries, buy and sell policies, and key-person policies that conform to the conditions as set out in the Act. It’s important to note that endowment policies (local and offshore) that don’t pay out on the death of a life assured, but are owned or part owned by a deceased policyholder, will be subject to estate duty. The surrender value of the policy must be included as property in the deceased estate.

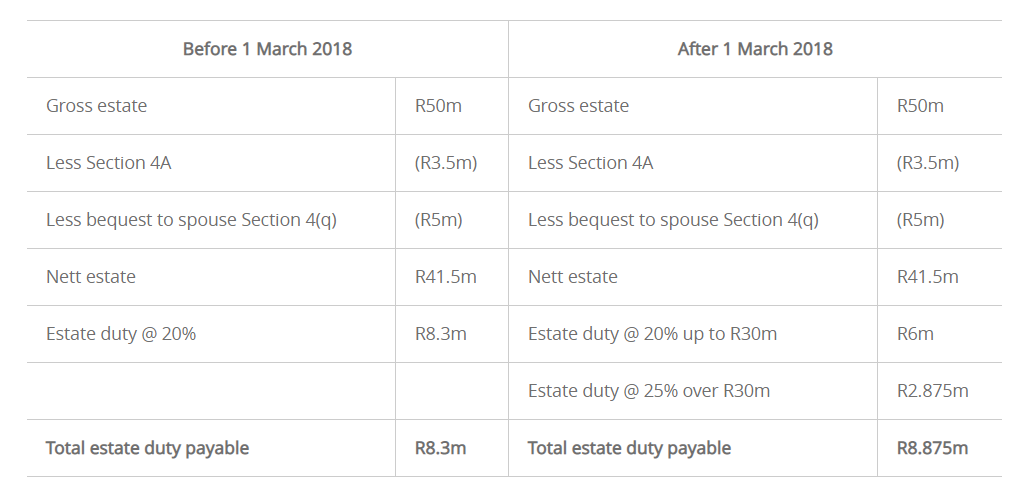

What are the practical implications of the estate duty rate increase as announced in the Budget Speech? The impact can be illustrated by the following example:

For an estate with a gross value of R50 million, with a bequest of R5 million to the surviving spouse:

The formation and registration of trusts, and the provision of independent trusteeships – both local and offshore.

The creation of BEE, charitable, special and Shariah trusts compliant with regulatory and legislative requirements.

The administration of deceased estates in South Africa and abroad.

Advice on complex structures, asset restructuring and bequests in foreign jurisdictions.

Advice on emigration and immigration, foreign earnings and the application of any double taxation agreements.

Updating trust deeds to ensure they’re in line with the latest changes in the trust environment.

Updating and/or drafting of wills dealing with South African and/or foreign assets.

Advice on the establishment and management of charitable organisations, their tax status and tax deductible donations.

Advice on the potential tax consequences and reporting obligations if you hold a US passport or green card, or if you have children living in the US.

Guidance on the financial implications of life-changing events, such as getting married, divorce or the birth of a child.

For further information or advice, please contact Ken Newport at kenn@privatewealth.sanlam.co.za or on 011 778 6659.

The formation and registration of trusts, and the provision of independent trusteeships – both local and offshore.

The creation of BEE, charitable, special and Shariah trusts compliant with regulatory and legislative requirements.

The administration of deceased estates in South Africa and abroad.

Advice on complex structures, asset restructuring and bequests in foreign jurisdictions.

Advice on emigration and immigration, foreign earnings and the application of any double taxation agreements.

Updating trust deeds to ensure they’re in line with the latest changes in the trust environment.

Updating and/or drafting of wills dealing with South African and/or foreign assets.

Advice on the establishment and management of charitable organisations, their tax status and tax deductible donations.

Advice on the potential tax consequences and reporting obligations if you hold a US passport or green card, or if you have children living in the US.

Guidance on the financial implications of life-changing events, such as getting married, divorce or the birth of a child.

Expert advice is crucial in dealing with cross-border estate and tax planning.

Stanley Broun has spent 13 years in Fiduciary And Tax.

Have a question for Stanley?