Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

Interest-free or low-interest

loans to trusts

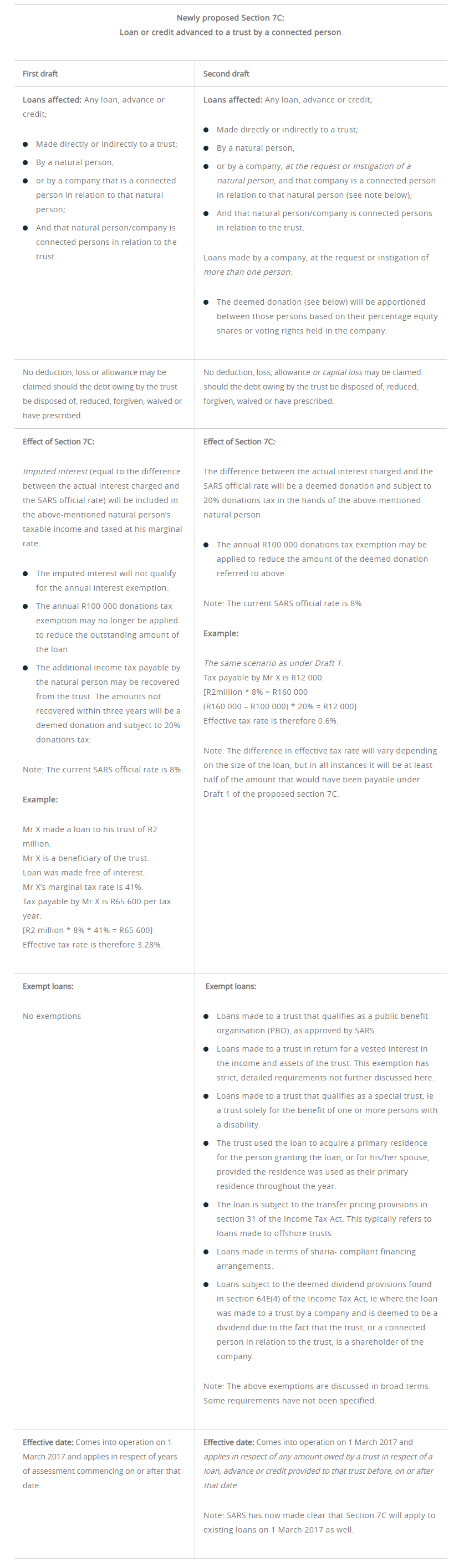

During the 2016 Budget Review, National Treasury proposed measures to combat tax avoidance through the use of trusts. The ‘first batch’ of the 2016 Draft Taxation Laws Amendment Bill (TLAB) was released for public comment on 8 July 2016. It contained proposals regarding the insertion of a new Section 7C to address interest-free or low-interest loans made to trusts.

These proposals caused quite a stir due to the significant increase in taxes relating to trusts that would arise. Many believed this was the beginning of the end of trusts, and again, players in the financial arena debated and questioned the future use of trusts.

Treasury released the ‘second batch’ of the 2016 Draft TLAB on 26 September 2016. Fortunately it appears to be a lot less harsh than its predecessor. It also appears as though many of the ‘inherent flaws’ of the first draft of Section 7C have been addressed in the second draft.

We have summarised the main differences between the first draft and second draft below:

The formation and registration of trusts, and the provision of independent trusteeships – both local and offshore.

The creation of BEE, charitable, special and Shariah trusts compliant with regulatory and legislative requirements.

The administration of deceased estates in South Africa and abroad.

Advice on complex structures, asset restructuring and bequests in foreign jurisdictions.

Advice on emigration and immigration, foreign earnings and the application of any double taxation agreements.

Updating trust deeds to ensure they’re in line with the latest changes in the trust environment.

Updating and/or drafting of wills dealing with South African and/or foreign assets.

Advice on the establishment and management of charitable organisations, their tax status and tax deductible donations.

Advice on the potential tax consequences and reporting obligations if you hold a US passport or green card, or if you have children living in the US.

Guidance on the financial implications of life-changing events, such as getting married, divorce or the birth of a child.

We recommend that you contact one of our Fiduciary and Tax team members to discuss your particular circumstances, as each case will need to be assessed on its own merits.The brunt of Section 7C appears to have been reduced significantly by its second draft. It’s also clear from the second draft that it provides more scope for estate planning so as to utilise the benefits of a trust in a cost-efficient manner. From the current wording, it also seems as though loans to companies will not fall foul of the provisions of Section 7C, which provides further planning opportunities.

The formation and registration of trusts, and the provision of independent trusteeships – both local and offshore.

The creation of BEE, charitable, special and Shariah trusts compliant with regulatory and legislative requirements.

The administration of deceased estates in South Africa and abroad.

Advice on complex structures, asset restructuring and bequests in foreign jurisdictions.

Advice on emigration and immigration, foreign earnings and the application of any double taxation agreements.

Updating trust deeds to ensure they’re in line with the latest changes in the trust environment.

Updating and/or drafting of wills dealing with South African and/or foreign assets.

Advice on the establishment and management of charitable organisations, their tax status and tax deductible donations.

Advice on the potential tax consequences and reporting obligations if you hold a US passport or green card, or if you have children living in the US.

Guidance on the financial implications of life-changing events, such as getting married, divorce or the birth of a child.

Expert advice is crucial in dealing with cross-border estate and tax planning.

Stanley Broun has spent 13 years in Fiduciary And Tax.

Have a question for Stanley?