Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

ALPHABET: AN

INNOVATOR OF NOTE

There have been several big winners in the artificial intelligence (AI) boom since the start of the year, with the leaders’ share prices spiking to record highs. One of our biggest holdings in this field is global technology company Alphabet Inc. We remain positive about this company’s prospects – in our view, Alphabet’s unparalleled technology platform and opportunities in multiple compelling growth verticals will enable it to generate free cash flow growth of high single digits over the next decade.

Alphabet has been an AI innovator for some years now, but AI is just one way in which the company is enhancing its business model over time. Its main business unit, Google, remains poised to benefit from the ongoing secular growth tailwinds in search and display advertising, as well the explosion of mobile users. In general, Google is uniquely positioned to outgrow the overall market due to continuous innovation in tools that should enhance its competitive position.

These often groundbreaking innovations include:

Google Maps: Since the early days of Street View, Google has stitched together billions of panoramic images so people can explore the world from their devices. One feature is Immersive View, which uses AI to create a high-fidelity representation of a place, enabling you to experience it before you visit. The scale on which Google Maps operates is simply breathtaking – it provides 20 billion kilometres of directions every day.

Google Photos: Another product made better by AI is Google Photos. Google introduced it in 2015 as one of its first AI-native products. Breakthroughs in machine learning have made it possible to search your photos for things like people, sunsets or waterfalls. More than 1.7 billion images are edited each month in Google Photos, and AI advancements have given users increasingly powerful ways to do this. For example, Magic Eraser, first launched on Google’s Pixel phones, uses AI-powered computational photography to remove unwanted elements in a picture.

PaLM 2: This stands for Pathways Language Model, version 2, and is a large language model (LLM) developed by Google AI. It is a successor to PaLM, which was introduced in 2022. This technology has far-reaching practical applications, including in the field of medical technology. Med-PaLM 2 enables fine-tuning in medical images and achieves a nine-times reduction in inaccurate reasoning when compared to the base model. It can synthesise information from medical imaging like plain films and mammograms.

Updates to Bard: Launched in March this year, Bard is Google’s experiment in the field of conversational AI. Bard supports a wide range of programming capabilities, and it has become much smarter at reasoning and maths prompts. It is now running on PaLM 2.

Alphabet is now trading at the most attractive levels in three years and given the quality of the business and its above-average growth prospects, we’re of the view that it shouldn’t be at a discount to the market. In its last quarterly update, Alphabet noted that in the face of an uncertain macro environment, Search remains resilient. It was pleasing to see a quarter-on-quarter increase in Search revenue.

GOOG reported Search & Other revenue of +2.1% year on year compared to the previous negative year-on-year rate. We expect Search & Other growth to accelerate as we progress through 2023. The PaLM model has enhanced Bard’s capabilities, enabling it to assist with programming and software development tasks, including code generation.

For developers, Alphabet released the PaLM application programming interface (API) to help programmers to start building generative AI applications more rapidly. The company has also improved bidding models to adjust for differences in search ad formats and has opened up the beta test for automatically created assets to all advertisers in English. In addition, Alphabet is bringing generative AI to customers across the cloud portfolio. All these new tools should enhance its competitive position.

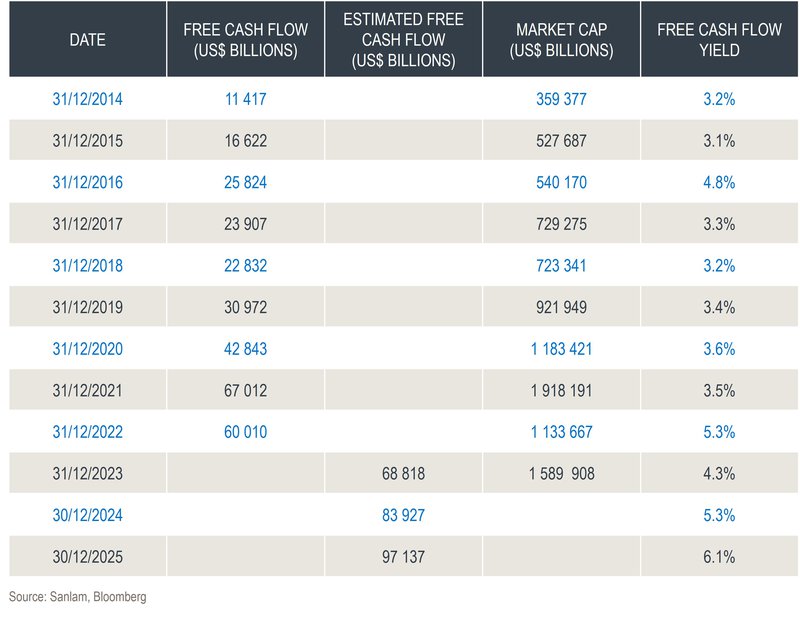

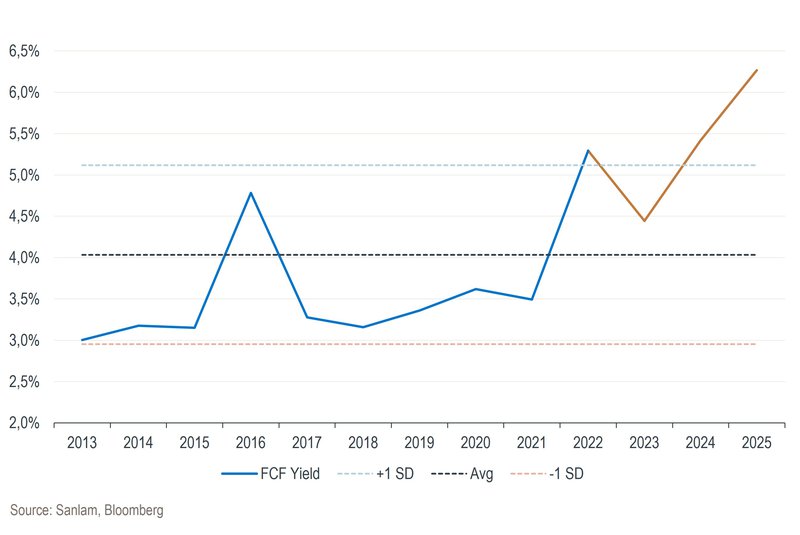

As can be seen on the table and the graph below, the free cash flow yield over time at each year end since 2014, when we first included Alphabet in the Sanlam Global High Quality Fund, shows that the stock was never in deep value territory. If the company can continue to grow free cash flow, the current valuation appears attractive based on a forward free cash flow yield of 6.1% by 2025.

Alphabet’s free cash flow, market cap and yield (2014-2025)

Free cash flow yield

We provide daily reporting of trades, monthly portfolio evaluations and annual tax reports to clients.

Looking for a customised wealth plan? Leave your details and we’ll be in touch.