Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

Central bank action:

does it influence our investment philosophy?

Central bank action – including quantitative easing – initiated to spur economic growth in the years following the 2008 financial crisis, has come under fire of late. It’s increasingly being perceived as being ineffective, driving inflation higher and negatively affecting markets. We asked Pieter Fourie, our Head of Global Equities at Sanlam Private Wealth UK, about the influence of central bank action on SPW’s investment philosophy and process.

Central banks seem to be stuck in a feedback loop of politics, economics and market vulnerabilities, with politicians now also joining a growing number of critics questioning persistently low interest rates. In Europe in particular, the dovish actions of the European Central Bank (ECB) will continue to influence other central banks and negative interest rates will continue to proliferate on the continent. ECB President Mario Draghi has postponed a decision on further quantitative easing (QE) to December, when updated macroeconomic forecasts and the conclusions of relevant committees working on QE implementation will become available.

Against this backdrop, central banks are likely to tread carefully when contemplating how soon to hike (US Federal Reserve), taper (ECB) or even take steps to increase monetary stimulus (Bank of Japan). Even though China’s policy-induced growth surge doesn’t look sustainable, Europe’s problems appear even more severe. Portugal may keep its investment grade status, but its banks remain impaired and its debt dynamics challenging. Italy is in a similar position. Europe’s fragilities are amplified by political risks: Greece has just begun a difficult programme review, Italy is approaching its crucial referendum and Spain still has no government.

All factors considered, we think European interest rates will remain on hold and the US Fed will raise interest rates in December. None of this drives our investment process per se – it will only influence our decision-making process if low interest rates lead to opportunities for us in the equity market.

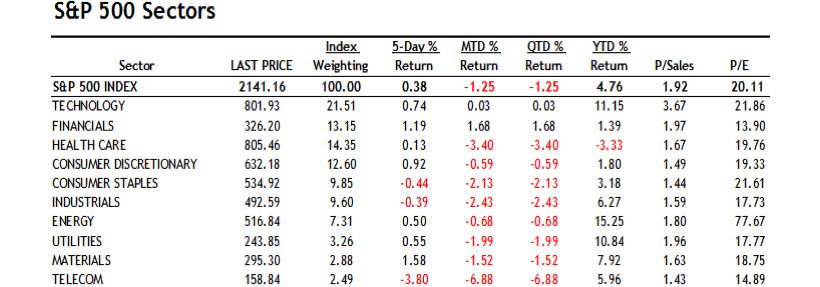

As can be seen on the table below, the technology, energy and utilities sectors have been the best performers in the US this year. We have no exposure to the last two, and one could argue that a low interest rate environment has helped the utility sector this year. We remain concerned about long-term fundamentals for most utility companies due to regulatory pressures.

On the flip side, we still see lots of opportunities for certain sectors within technology to keep growing while using strong free cash flow to reinvest back into their businesses or return cash to shareholders. Names that performed well for us this year include Alphabet, PayPal, Samsung, Microsoft and Oracle.

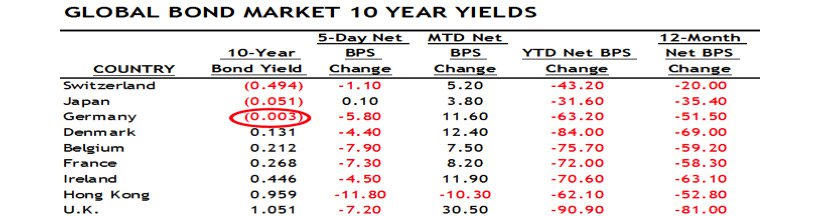

Global bond yields continue to be extraordinarily low, as the table below illustrates.

The reason equity valuations in ‘bond-like’ equity proxies are high is perhaps because bond investors are flocking into these names and pushing valuations higher even when earnings growth is weak. It should come as no surprise that over the past two years we’ve sold names such as Louis Vuitton, AB InBev and British American Tobacco as valuations reached unsustainable levels.

Looking at the growth prospects of consumer staples, our short-term, more negative view has been reinforced by evidence from the third quarter reporting season, as multinational staples companies grapple with slower emerging markets, more competition and developed market disinflation, causing earnings per share growth to fall to a 20-year low. Over the past two years we’ve substantially reduced our consumer staples exposure in favour of an increased healthcare position.

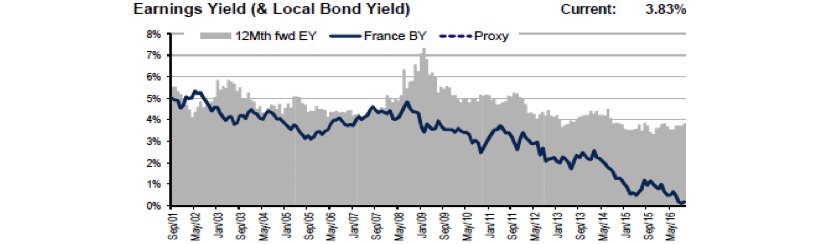

French company Essilor is the leading player in a market that should generate decent defensive growth over the longer term. The company produces a range of lenses to improve and protect eyesight, as well as optical equipment. While this growth is defensive, it’s also relatively modest. Essilor has boosted its organic growth through mergers and acquisitions as it continues to consolidate a fragmented market.

Looking at the valuation below one could argue that a 3.83% free cash flow yield is attractive versus local French bond yields at barely 50 basis points. However, as equity investors, it would be foolish to measure equity risk against a potential bond bubble in sovereign European debt. We therefore prefer to remain on the sidelines for many European high quality names like Essilor, even when the growth prospects appear rosy over the long term.

European banks look extraordinarily cheap on a relative basis and following a period of severe underperformance due to money-printing activities globally. These monetary efforts have compressed interest rate margins for the banks and caused earnings to collapse. We continue to avoid the banking sector until such time as we become more confident that Europe can withstand a higher interest rate environment.

Medical care consumer price index (CPI) inflation has accelerated sharply this year. The increase is broad-based across medical goods and services. We think the rise in medical CPI is being driven by structural shifts in the healthcare sector. We’re exposed to healthcare at a sector level through both drug companies and medical equipment companies and are looking for opportunities to reinvest in names like Stryker on any pullbacks. Our list of top positions also reflects our ‘healthy’ health exposure to an industry we perceive as a solid growth sector over the long term.

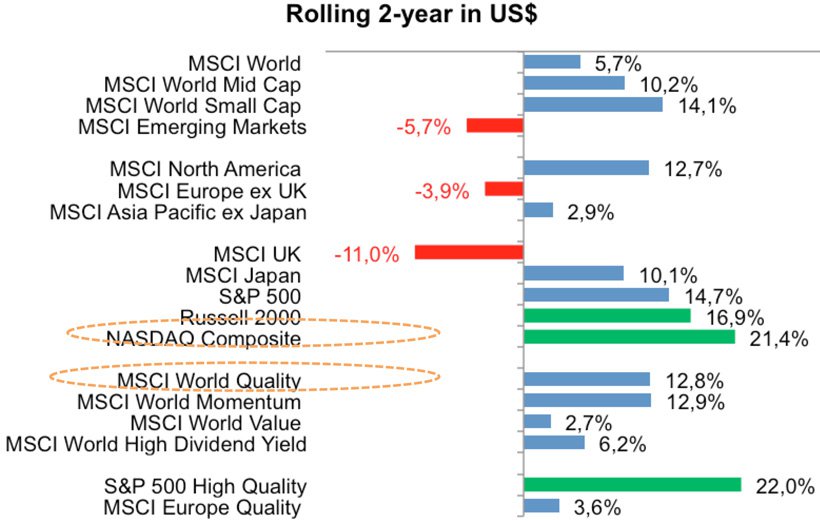

Many investors favoured Europe and the UK over the past two years, but we’ve been consistently underweight in both these regions, on a combined weight. As shown on the table below, the Nasdaq performed well and through companies like Alphabet and Microsoft, two names we continue to favour, we remain invested in that part of the market with secular growth dynamics even as these names reach new all-time highs.

Over the past six months, emerging markets have performed well after 18 months of severe underperformance. We’ve sold positions such as NetEase and Samsung after strong moves of 40% or more in US dollar terms on average, having built up these positions when valuations were low.

Our core positions continue to favour companies with pricing power, strong balance sheets and decent growth prospects while trading at attractive valuations. Positions are diversified among sectors we continue to believe will have good growth prospects over the long term, irrespective of the macro environment. Examples are:

We constantly challenge the norm. Our investment process is a thorough and diligent one.

Michael York has spent 21 years in Investment Management.

Have a question for Michael?