Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

GOLD: TO BUY

OR NOT TO BUY?

We all know that discussing politics or religion at the dinner table is a sure way to ruffle feathers and even ruin the get-together. The same may be said of any debate about whether gold should be included in an investment portfolio. Views on this subject tend to be highly polarised – investors seem to either love gold, or they’ll never be persuaded to buy it. We set out our objective assessment of the investment merits of the precious yellow metal.

The story of gold begins nearly 5 000 years ago, with the first records of the monetary use of precious metals dating to the Early Bronze Age around Mesopotamia and Egypt. Gold became valuable during this time since it was useful as a medium of exchange to facilitate commerce, it was an effective store of wealth for the upper class and, importantly, it was a radiant display of power and status for the ruling elite of the state. While it’s no longer a common medium of exchange, the precious metal still has merits as a store of value in investment portfolios.

Today gold needs to compete with traditional asset classes for ‘shelf space’ in an investment portfolio. Crafting the proportions of the broadly defined asset classes – equities, cash, fixed interest assets, property and alternative investments – is based on the valuation, or the implicit prospective returns, and the risk associated with each asset class. The relative attractiveness of an asset class should, all things being equal, determine its weight in a portfolio. To reduce risk we introduce diversification or create a blend of different asset classes – their respective price behaviours would typically be uncorrelated and hence provide a less volatile investment return outcome.

Since equities, property and fixed income assets generate an income, it’s possible to determine a value for these asset categories based simply on the expected income stream. Gold does not generate any income. We therefore find it extremely difficult to put a value on the metal, and are hesitant to add it to our clients’ portfolios – its inclusion would depend largely on the hope that another investor would in future believe the investment is worth more than what we paid for it.

In our view, there are two ways to think about the value of gold. The first relates to its scarcity value. If you buy gold because it is scarce, then the price should be closely related to the marginal cost of producing the metal. However, the price history of gold since 1974 – the first year it was freely traded in recent history – suggests that there’s no reliable relationship between the traded value of gold and the marginal cost of production. A decision to put value on gold based on this cost wouldn’t have produced good investment results for portfolios. For the record, the marginal cost of production is currently around US$1 400 per ounce versus a traded gold price of US$1 950 at the time of writing.

The second reason for considering gold – and why we would recommend a holding in the metal – is that it’s widely believed to be a store of value in times of uncertainty, or when the purchasing power of money deteriorates – in other words, when there is inflation.

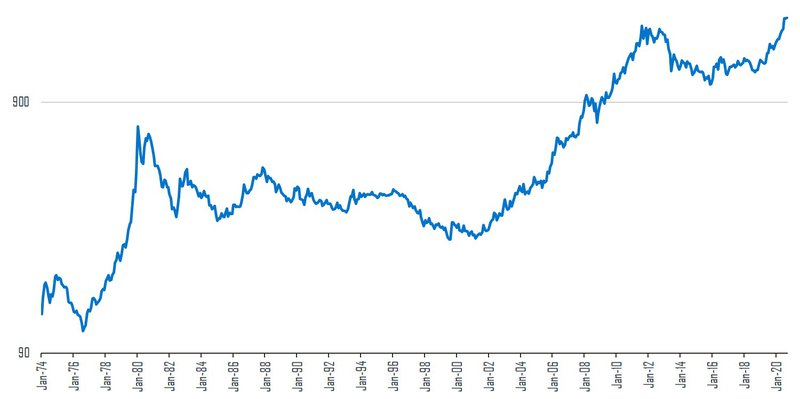

The gold bulls often use this argument which, in our view, should be put to the test. It’s clear from the graph below that gold performed well from the mid-1970s to the early 1980s when the world was plagued by a high inflation rate triggered by an oil shock. But then the gold price traded sideways for more than 20 years, and investors lost faith in the metal as an investment. In fact, it was only in 2007 during the global financial crisis that gold reached the highs of 1980 again and since then, the uncertainty in the macro arena has certainly added to the attraction of the metal.

Dollar gold price

Source: iNet

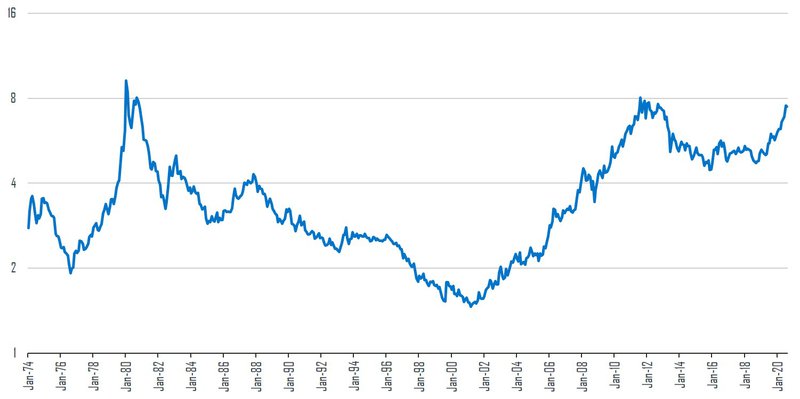

When we look at a similar graph in real terms (after inflation), the case for gold as an investment looks patchy, yet it managed to outperform US inflation since 1974. One can’t deny the fact that there have been periods over the past 46 years when an investment in the precious metal has rewarded investors richly.

Real dollar gold price

Source: iNet

The gold price behaves in a way uncorrelated to equity prices. In an investment landscape of highly volatile global equity markets, it therefore makes sense to include the metal in our clients’ portfolios, as it is likely to reduce volatility in overall investment outcome.

Given the unique global macro-economic environment investors are currently experiencing, gold is now on our investment radar. It could be reasoned that we should have invested in gold earlier, when it became obvious that the COVID-19 crisis would support the gold price and have a negative impact on other asset classes. Why didn’t we? To answer this question, we need to share our views on the structuring of our multi-asset or balanced portfolios.

In late 2019, we were concerned about the value and therefore the prospective returns of global equities. We trimmed our global equity exposure and left the proceeds in cash to provide optionality. When COVID-19 struck, the portfolios were relatively defensively positioned – they have, in fact, outperformed those of our peers.

In hindsight, exposure to gold would have done better than cash in the portfolios, but no one could at that stage predict the outbreak of a global pandemic. In the midst of the crisis, we decided to reinvest in the equity market as valuations were then attractive on longer-term views. We chose not to buy gold as it would have been an ‘after the fact’ investment. The subsequent rally in global equities from the lows in late March has justified our decision to add risk during the sell-off and has allowed us to trim global equity exposure once more, as we believe this recovery may be too strong, too quickly. Having said that, the gold price also firmed even as equity prices rallied off their lows.

The higher cash levels currently in our clients’ portfolios now pave the way for a potential gold investment. In our view, there are a number of potential macro outcomes likely to support the case for an investment in the precious metal:

Most of these arguments should be well known to investors and this may well explain the recent strength in the gold price. However, they’re likely to remain valid for the foreseeable future. Should the gold price pull back from its current high level, we are therefore likely to add to the metal in our clients’ multi-asset portfolios.

When formulating your investment strategy, we focus on your specific needs, life stage and risk appetite.

Looking for a customised wealth plan? Leave your details and we’ll be in touch.