Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

HOW DO FALLING RATES

AFFECT THE BANKING SECTOR?

As inflation reaches central bank targets and we transition into a period of easing interest rates globally, the effects are likely to ripple across economies and, in turn, impact investment markets. In South Africa, a reduction in interest rates will help alleviate pressure on consumers and stimulate economic growth. For banks and investors in the sector, however, a different set of challenges and opportunities arise. What does a falling rate environment mean for our banking sector, and where might investors find growth and stability?

South Africa’s banking industry is led by major players Standard Bank, FNB, Nedbank, Absa, Capitec and Investec – the first four accounting for 90% of South African loans and deposits. These banks, known for their conservative approach, have demonstrated resilient earnings and maintained strong capital positions – their reputation solidified by their ability to withstand multiple financial crises such as the Covid-19 pandemic.

However, they’re not immune to the macro environment, including the effects of changing interest rates. Since 2020, we have witnessed these businesses enjoy a stellar recovery, exceeding their 2019 earnings bases. Among the drivers of this recovery were the benefit of rising interest rates and the positive endowment effect. However, along with this tailwind for earnings came the negative impact of increased defaults by borrowers.

South Africans have experienced rising interest rates over the past few years, with most observers of the view that we’re currently at the top of the rate cycle. With inflation starting to come under control, the South African Reserve Bank has begun to slowly shift gears. This pivot towards lower rates encourages borrowing and increased spending, giving businesses room to invest and expand. But what does it mean for banks – and crucially, for those invested in them?

While rate cuts can boost economic activity, they also squeeze margins, influencing profitability and how banks grow their loan books. The relationship between falling rates and bank profitability is complex.

An immediate impact of lower interest rates on banks is a squeeze on their net interest margins (NIMs) – the difference between what they earn on loans and what they pay on deposits. In a falling rate environment, the rates banks charge on loans drop since many are variable-rate, prime-linked loans rather than fixed-rate loans. While deposit rates are also expected to drop, we believe that the current environment is highly competitive as banks compete for customer deposits and loans, which will see NIMs narrow and impact profitability.

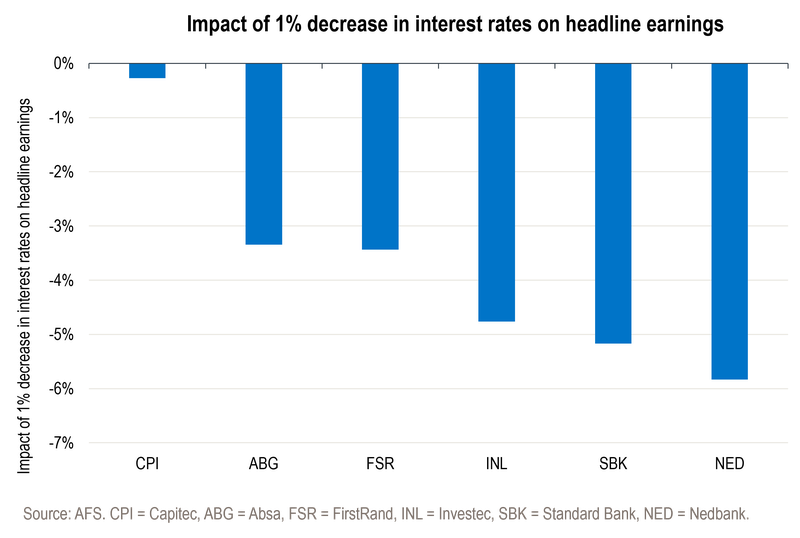

The graph below provides a simple illustration of the sensitivity of earnings due to declining rates:

As can be seen on the graph, a reduction in interest rates affects each bank individually. According to our calculations, Nedbank’s earnings are the most sensitive to a 1% reduction in interest rates, resulting in a 6% decline. This sensitivity can be attributed in part to its business composition and current lack of an interest rate hedging strategy, unlike Absa and FirstRand. Consequently, during the period of rising interest rates, Nedbank’s margins expanded, offsetting the impact of credit losses and supporting robust earnings growth.

In contrast, Absa implements an interest rate hedging strategy aimed at maintaining stable margins across different interest rate cycles. While this approach has limited the benefits to Absa during rate hikes, it does mean the bank faces less earnings pressure as interest rates decline. Similarly, FirstRand shows lower sensitivity to interest rate fluctuations, reflecting a comparable stability in earnings under shifting macroeconomic conditions.

While Standard Bank has recently implemented a hedging strategy for its South African loan book, which has reduced its sensitivity over the past 12 months, a large portion of the bank’s business is from the rest of Africa, which is not hedged.

Investec has no hedging strategy in place for either its local or its UK business. While we’re illustrating the headwind on earnings for a 1% reduction in rates, it must be noted that 50% of Investec’s earnings and loan book are from the UK. If the UK starts to normalise interest rates, it could reduce rates by much more than 1%, posing an even greater risk.

On the upside, lower rates often stimulate demand for loans, especially in the home loans and consumer lending segments. Lower borrowing costs make debt more attractive for individuals and businesses. They also enhance credit affordability, thus supporting banks in expanding their loan portfolios. This increased lending activity can offset some of the NIM compression, particularly for banks with strong retail portfolios, which can benefit from a lending and transactional banking perspective.

In addition, debt servicing becomes easier as interest rates fall, and the risk of default generally decreases. This means banks may not need to set aside as much in provisions for bad loans, which can improve profitability. For investors, this can signal a more stable income outlook from banks as the risk of credit losses falls, potentially improving earnings visibility.

Stable margins and improved credit losses are particularly relevant for Absa at the moment. The bank is poised to benefit from lower rates, but it can show better earnings growth than peers as its credit losses unwind from elevated levels over the next 12 months, especially within its large retail business.

FirstRand is well positioned to navigate shifts in the interest rate environment. Its high-quality loan portfolio, proven capacity for deposit growth and robust retail business make it well equipped to capitalise on an improving consumer landscape in South Africa. Additionally, FirstRand’s ongoing focus on revenue diversification through cross-selling, insurance, and wealth and investment services further strengthens its strategic outlook.

The prospect of falling interest rates is shifting the landscape for South African banks. By keeping an eye on which banks are best positioned to leverage a lower-rate environment, investors can make more informed decisions, balancing short-term challenges in the industry with long-term growth potential.

Your wealth plan is designed with you in mind. Your financial reality, aspirations and risk profile.

Carl Schoeman has spent 22 years in Investment Management.

Have a question for Carl?