Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

MTN:

making the correct call

At Sanlam Private Wealth (SPW), our investment approach has always been to craft diversified portfolios of assets that collectively outperform over the long term (at least five years), and to avoid the distraction of quick wins. In the process, we’ll sometimes own unpopular stocks, and like all asset managers, might from time to time err on an individual share. But as professional investment managers, we don’t get too excited about short-term gains and losses, or too caught up in the ‘noise’ impacting a particular stock. With all the news hype around MTN of late, however, we’d like to clarify our position on this share.

When we at SPW select equities, we seek companies capable of delivering earnings and dividend growth at attractive valuations. Crucially, we want to make investments in companies in which we believe through an investment cycle, rather than speculating on short-term price movements.

When we initially bought leading telecom operator MTN in 2003, we believed it provided exposure to growth in consumer spending in Africa’s biggest economies (the company’s operations span 22 markets, including South Africa and Nigeria) in an area in which most would regard the spend as ‘compulsory’ due to a lack of alternatives in these jurisdictions.

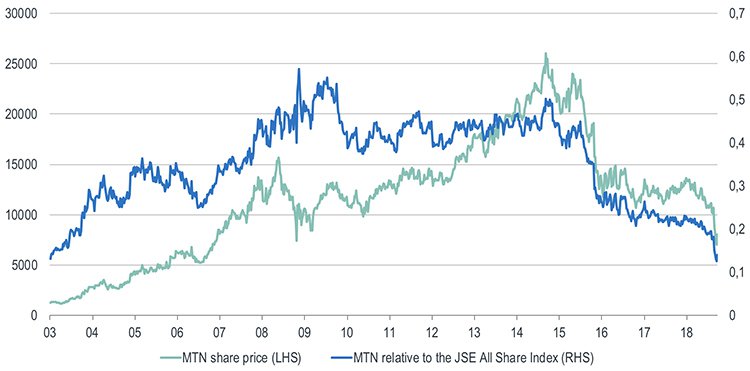

Was it the correct call? The following chart, setting out MTN’s performance relative to the JSE’s All Share Index (ALSI), provides the answer:

As the chart shows, the MTN share price performed particularly well until 2008. From that year, the momentum of the outperformance came off, but the share still outperformed until early 2015. Unfortunately, from then onwards, it underperformed significantly and within three years, all the gains accumulated over the previous 12 years were wiped out. It’s not unfair, then, to say that our call on MTN has been incorrect since early 2015.

Back in 2014, when we believed MTN’s growth pattern was slowing, we undertook an in-depth analysis of the company. We arrived at a valuation of just over R200 per share, which represented a substantial gap between the traded share price and our intrinsic value of it.

A series of problems, many outside the control of the company’s management, followed. The oil price declined and the Nigerian naira came under severe pressure. In South Africa, Cell C caused a price war, and management issues within MTN followed. In Nigeria, MTN was heavily fined when the company missed the deadline on regulatory issues.

Then last month, the Nigerian Central Bank charged that MTN had illegally transferred US$8 billion out of the country. In our view, this claim is irrational and quite frankly, opportunistic, but it nonetheless led to the price of MTN shares falling by more than 30%. The latest developments seem to indicate that a ‘resolution’ might yet be reached between the telecom operator and the Nigerian authorities, which in turn, has had a positive impact on the share price.

A common criticism levelled against asset managers invested in MTN, including SPW, is that we don’t fully appreciate the risks of doing business in Africa. At SPW, we follow a specific process in terms of how we evaluate companies, based on our expectations of future cash flow. We always use punitive discount rates when we value companies operating in frontier markets. In other words, we value these businesses as if they’re materially riskier than those operating in South Africa.

It’s of course impossible to ‘model’ for the irrational behaviour of certain African authorities as a base case. If we had to make allowance for this, we wouldn’t be able to invest in any company doing business in Africa – including shares such as the major banks, Shoprite, Vodacom and AB InBev. In short, our view was that the risks associated with MTN were already discounted in the share price.

Investing in equities is always risky, but the uncertainty associated with this asset class also often creates interesting investment opportunities. We do need to mitigate against these risks, however, which is why it’s crucial to craft a diversified portfolio of assets that will collectively outperform a benchmark and competitors over time.

Our investment returns bear this out – our South African equity model portfolio has delivered an annual return of 11.8% against the ALSI’s 9.8% per year over the 10 years to August 2018. Our equity fund recorded a performance that puts it in the top 20% against competitors over the past five years (we don’t have a 10-year track record for this fund).

But back to MTN. Over the past few weeks, we’ve been asked by concerned investors whether they should sell their MTN shares. In our view, the correct question to ask instead is whether or not to buy the stock. Our current valuation of the share would suggest that in isolation, it offers material upside. However, we need to answer this question within the context of our equity portfolio as a whole, in which we also have cyclical shares such as Anglo American, Billiton and Sasol. With high forecast risk in terms of commodity prices, we’re hesitant to accommodate more risk in our clients’ portfolios and increase exposure to MTN now.

Should the share price come under further pressure, the so-called margin of safety will increase. Under these circumstances we may consider adding to our MTN stock. It remains a good business. After the management team refresh in 2016 and 2017, most of the top 30 managers have been in their positions for over a year now. The wide footprint MTN has in both South Africa and Africa adds further credibility to the share’s investment merits.

We constantly challenge the norm. Our investment process is a thorough and diligent one.

Michael York has spent 21 years in Investment Management.

Have a question for Michael?