Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

Old Mutual:

has unbundling benefited shareholders?

Old Mutual officially returned to its African roots on 26 June this year, when Old Mutual Limited started trading on the JSE, where it now has its primary listing. Quilter PLC was unbundled to Old Mutual shareholders during the same week. Last month, we argued that the so-called ‘managed separation’ of Old Mutual should be beneficial for shareholders. How has this played out so far?

Former Old Mutual PLC shareholders would have received one Quilter PLC share and three Old Mutual Limited shares for every three Old Mutual PLC shares owned. We can therefore compare shareholders’ current position to their pre-unbundling position by adding a third of the share price of Quilter PLC (currently R27.40) to the share price of Old Mutual Limited (currently R28.90).

At the time of writing this equated to R38, which, importantly, is still 5% below the R40 share price that Old Mutual PLC was trading on back in March 2016 when it announced it would be embarking on the separation. Shareholders have therefore not seen any benefit from the promised value unlock – in contrast to a number of lawyers and investment bankers who assisted with the process.

Despite our disappointment with the lack of shareholder wealth creation so far, we do believe Old Mutual Limited is currently undervalued and that the cleaner structure, potential for return of capital, and future unbundling of Nedbank will lead the market to ascribe the appropriate value for Old Mutual Limited over time.

The separate listings of Old Mutual Limited and Quilter have resulted in the exclusion of these shares from large developed market indices like the UK FTSE 100. This has likely created short-term selling pressure on the shares as index tracking funds were forced to sell them irrespective of their perceived value.

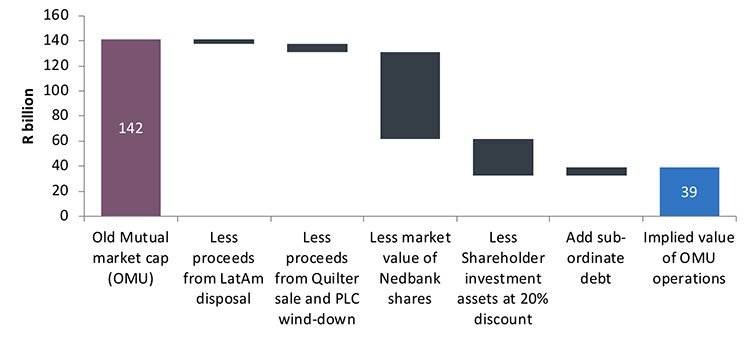

One way of looking at Old Mutual Limited’s current valuation is to strip out the following items from its market cap to derive the market-implied value for the local insurance, lending and asset management operations (Old Mutual Limited operations), as depicted in the graph below:

Nedbank’s value is based on its current listed market value, while the other assets are or will be liquid assets, so the valuations of these are quite straightforward. Stripping out these assets, we calculate a market-implied value of R39 billion for the Old Mutual operations.

After adjusting for disposals, additional operating cost as a stand-alone business, minorities and targeted cost savings, we estimate that these operations should generate around R7.8 billion in profit after tax this year. In effect, investors are therefore picking up the Old Mutual Limited operations at a five-times normalised price-to-earnings (PE) ratio, which is a material discount to its competitors. Sanlam, for example, trades on a 15-times PE.

Old Mutual will unbundle around 33% of its 53% stake in Nedbank over the next six months. We further hope that Old Mutual’s management will distribute the proceeds of LatAm, Quilter and the residual PLC to shareholders as a special dividend or share buyback over the near term. This should place more emphasis on the attractive valuation of the Old Mutual Limited operations and finally unlock value for shareholders.

We can help you maximise your returns through an integrated investment plan tailor-made for you.

Niel Laubscher has spent 10 years in Investment Management.

Have a question for Niel?