South Africans can purchase property in Mauritius only in one of the approved Integrated Resorts Schemes and Real Estate Schemes – sometimes jointly referred to as Property Development Schemes (there’s also an Invest-Hotel Scheme (IHS) for hotel developers, not covered here). Deciding which property to buy is only the first of a number of decisions you need to make, however. A key decision is the form of ownership you’d like – there’s no one-size-fits-all solution.

When buying property in Mauritius, you must consider:

PERSONAL REASONS AND INTENTIONS

- Is this purely an investment? Do you intend to let the property, or is it for personal use only?

- Are you planning to relocate or emigrate to Mauritius at some point?

- Are you currently a South African tax resident and will you remain one for the foreseeable future?

- Do you have other offshore assets in your portfolio, and what existing structures – if any – do you have in place to house these? Do you intend to grow this international asset portfolio?

- What is your family situation? Are you single, married or divorced? Do you have young children? Minor children can live in Mauritius under your residency permit but will need their own once they reach the age of 18

- How many days a year are you intending to be resident in Mauritius?

MAURITIAN FACTORS

- Non-citizens of Mauritius can only buy into one of the approved development schemes

- Ownership can only take place directly as an individual, or via a recognised Mauritian entity, such as a Mauritian trust, Mauritian domestic company, or société

- As a general rule, a property investment equal to or exceeding US$500 000 gives the investor access to a residency permit. Only Integrated Resorts Schemes have a minimum required purchase price of US$500 000. Real Estate Schemes and Property Development Schemes don’t have a minimum purchase price, but remember that if you buy a property for less than US$500 000, this won’t get you residency

- Properties can be bought through vehicles such as trusts and companies, and residency permits can be passed on through these structures

- Mauritius has many tax-planning advantages to consider:

- No capital gains tax

- No inheritance, wealth or gift tax

- Flat 15% individual tax rate

- Corporate tax rate of 15% or lower

- No exchange control

- Strong tax treaty network

- No dividend, interest or royalties withholding taxes.

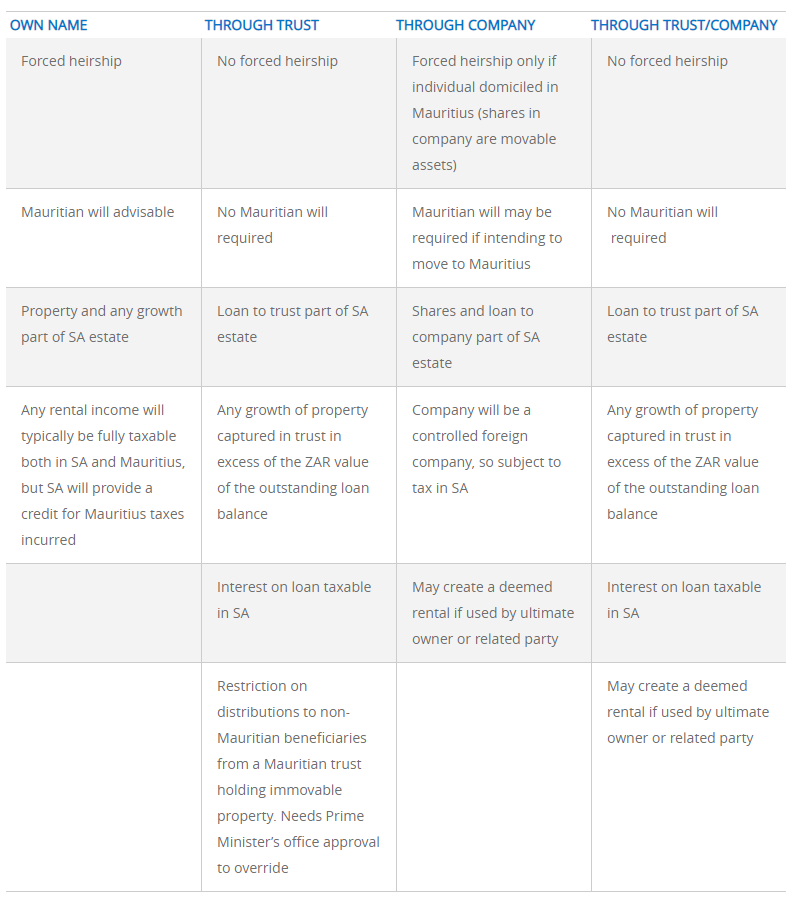

- While there may be no inheritance tax in Mauritius, there are ‘forced heirship’ rules that you need to understand properly before making any decisions. Essentially, they mean you’re not completely free to decide how your assets are disposed of upon death. A certain portion will be reserved for your heirs. The unreserved portion may, however, be freely bequeathed to any person or entity. This reserved portion varies depending on the number of heirs you have, and it’s important to note that this does not include your spouse. Immovable property in Mauritius is governed by this law, and movable property can also be affected depending on the last domicile of the deceased

- It’s therefore advisable to draw up a Mauritian will to deal with the ‘unreserved portion’ of any assets affected by the Mauritian succession laws

- In Mauritius, a loan to a Mauritian trust or company (to buy the property), and the shares in the company, are both considered movable assets.

SOUTH AFRICAN FACTORS

- South Africans investing offshore need to be aware of SA rules and how these will impact any offshore investment, including buying property in Mauritius

- If you purchase a property in your own name, it’ll form part of your estate. This means you’ll need to keep the Mauritian forced heirship rules in mind when drafting your South African will, and estate duty will be payable on it in South Africa – in Mauritius, there’s no estate duty

- If you buy the property through an offshore trust, then estate duty is payable on the value of the loan account (a trust will typically be funded from South Africa via a loan from the settlor of the trust). The loan will need to have an interest rate attached to it, and tax on the interest on the loan will be payable in South Africa

- If you buy the property through a Mauritian company owned directly by a South African resident, the shares in the company will form part of your estate in South Africa – they won’t be subject to Mauritian succession laws, as they’re movable assets of a non-Mauritian resident

- South Africa’s exchange control laws are also a consideration before moving money offshore.

The four structures most South Africans consider when purchasing a property in Mauritius are:

- Directly in your own name

- Through a Mauritian trust^

- Through a Mauritian domestic company* owned in your own name^

- Through a Mauritian domestic company* owned by a non-Mauritian (and non-South African) trust^.

* = A Mauritian société can also be used to replace the Mauritian domestic company, but this option is not covered here.

^ = If a special purpose vehicle (SPV) has been structured for the express purpose of avoiding the mandatory provisions of the forced heirship rule in Mauritius, the structure could be challenged and seen as a sham, which would make the Mauritian laws of succession applicable.

There are no hard and fast rules in terms of which option to choose, and each situation needs to be assessed on its own merits. Here are some examples:

- An individual has no concerns about the property forming part of a South African estate as they’ve already emigrated from South Africa and will move to Mauritius soon. They have no issues with the forced heirship rules in Mauritius and how these apply as they have only one child who will inherit everything. In this case, buying in their own name could work

- If an individual has no concerns about the property forming part of a South African estate as they intend to emigrate – but don’t want the forced heirship rules in Mauritius to apply – then buying through a company in their own name could work

- If an individual doesn’t want the property to form part of their South African estate, then an offshore trust is required. Any loan to the trust from a South African tax resident would form part of their estate and tax would be payable on the interest of the loan

- A Mauritian trust by itself can work if there’s no intention to make any distributions to beneficiaries, as there are restrictions in Mauritius – but a stand-alone trust that holds only the property could also work

- A trust with an underlying company is by far the best long-term solution, but it does carry the highest cost and may still be subject to a deemed rental in Mauritius if used by a related party for no rent

- If an individual intends to rent out the property, then owning it through a company works well

- If an individual has many assets worldwide, then housing these in an offshore (non-Mauritian) trust that owns a Mauritian property through a domestic company works well.

If you have any questions about buying property in Mauritius, please call Nick Jeffrey on 021 672 1865 or email nickj@privatewealth.sanlam.co.za.