Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

CHEAP SHARES: ARE THEY

ALWAYS A BARGAIN?

At Sanlam Private Wealth, our investment philosophy guides us to buy companies at prices below our assessment of their intrinsic value. This means that shares will come onto our radar if they underperform for some time and the price looks attractive. However, a stock is of course only a bargain if it will eventually cease being one. How can we ensure we invest in the ‘value plays’ and avoid getting caught in the ‘value traps’ – companies whose cash-generating power becomes permanently diminished?

While we don’t see ourselves as ‘value’ investors at Sanlam Private Wealth, we do know the future is far from certain, and thus prefer to have a wide margin of safety when buying shares. We typically prefer stocks that are inexpensive relative to our assessment of their fair value. But, of course, it can’t only be about price – we have a definite quality bias in that we always assess whether we would still be proud to own the company 10 years from now.

The key question is whether or not a company has the ability to grow its intrinsic value over time. And more importantly, whether the business can generate returns in excess of its cost of capital. It stands to reason that if a stock remains a bargain in perpetuity, an investor will only see returns from dividends and growth in the underlying earnings. For example, if a stock trades at a cheap-looking 7 times price-earnings (P/E) multiple, grows at 5% per year and pays out half its earnings as dividends, but does not re-rate, then an investor will only make an 11% internal rate of return (IRR), which is below the required return for local equities. For such a company to be a worthwhile investment, its rating would need to increase.

What this means is that before we buy into a ‘cheap’ company that might look like a ‘value play’, we have to ensure that we won’t get caught in what may turn out to be a ‘value trap’ in the long run – in our view, a firm or industry whose cash-generating power has been impacted more or less permanently.

While this may seem obvious, the market is littered with stories of businesses that went into slow decline and never succeeded in clawing their way back up – Kodak is one such example. Over the past decade, such giants as Ford Motor Company and General Electric have delivered negative total returns, and over the past five years, Deutsche Bank and Bed Bath & Beyond have delivered total returns of worse than negative 60%.

An examination of these firms’ earnings history shows they have been in decline for some years. At Sanlam Private Wealth, we believe there is only one way to avoid such potential market pitfalls – by engaging in the deep, fundamental research required to determine not only where a company’s earnings might go, but also where the long-term risks lie. We prefer to invest in companies that have a history of sound financial performance and sustainability, strong cash flow, and strong fundamentals.

On a more practical note, the following will also assist investors in avoiding being caught in a value trap when considering a particular share:

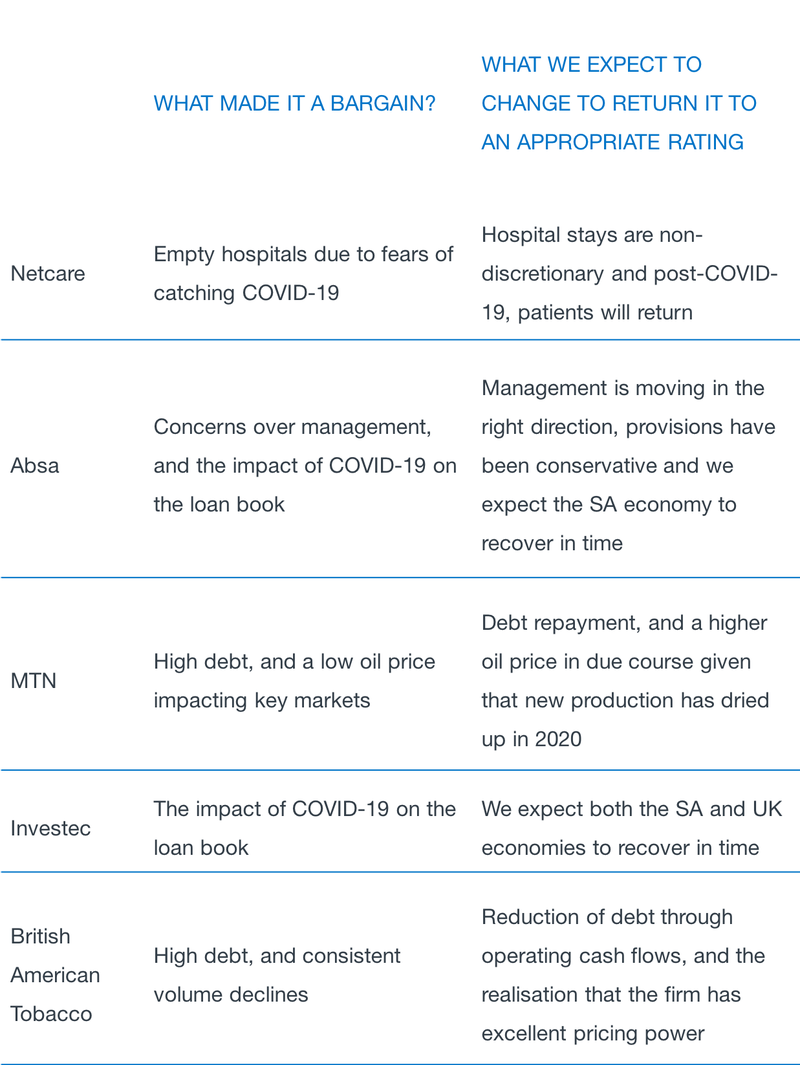

The bottom line is that when considering a company that appears to offer value, it is crucial to understand both what made it a bargain in the first place and what needs to change in order for it to no longer be a bargain. As an example, the table below shows some of this year’s purchases in our clients’ portfolios. While each company was, of course, the subject of thorough fundamental research by our investment team, the table indicates – at a very high level – our views on what made these companies attractive, and what changes are likely to positively impact their long-term earnings.

In line with our investment philosophy, valuation will always be top-of-mind when we at Sanlam Private Wealth build an investment thesis around a particular company or share. This can never be a one-off event, however – our investment team is continually reassessing all our investments to determine not only whether they are valued appropriately, but also whether their business models are sustainable for the long term.

Your wealth plan is designed with you in mind. Your financial reality, aspirations and risk profile.

Looking for a customised wealth plan? Leave your details and we’ll be in touch.