Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

EARNINGS GROWTH CRUCIAL FOR

SUSTAINED EQUITY PERFORMANCE

Looking back at the performance of financial markets in 2021, most investors would agree that a year of high double-digit US dollar returns from global equities exceeded expectations in an environment littered with so-called known risks. However, for sustained strong performance by this asset class, company earnings will need to grow in 2022, since the rating of global equities is unlikely to support the bull market into the new year.

Equity prices are driven by two main variables. The first is change in investor sentiment, also known as the ‘rating change’ of the asset class. This change in rating generally refers to the price-to-earnings (P/E) multiple of the market. When the P/E multiple increases, investors are prepared to pay a higher price for the underlying performance or earnings of the company.

When the P/E multiple is high relative to historic measures, it’s normally a reflection of a positive investment environment. The risk for investors is extrapolating this environment into perpetuity in their expectations. We therefore normally don’t factor in further re-rating when P/E multiples are high, as we know investor sentiment is likely to follow investment cycles – this has been the case throughout history and is unlikely to change in future.

The second driver of equity prices is growth in reported earnings or profits generated by companies that constitute the equity index. During the second quarter of 2020, company earnings worldwide came under pressure as a result of Covid-19 lockdown measures, which were dire for some industries – think hospitality, airlines and related sectors. Investors were rational when they sold down the prices of companies operating in these sectors.

The opposite also held true – the share prices of companies less affected by the lockdown measures were rather resilient, despite the general uncertainty caused by the outbreak and spreading of the virus.

We witnessed a remarkable recovery in global economic activity in the second half of 2020, following unprecedented monetary and fiscal stimulus introduced globally. This stimulus and, of course, the introduction of vaccines, created an environment in which company earnings recovered in a V-shape pattern off a low base. The resultant recovery in equity prices is now well documented.

But let’s look at the actual numbers over the past year. Looking at the biggest single stock market constituent of the MSCI World Equity Index, the US equity market, the S&P 500 advanced strongly by 28% over the 12 months ending on 30 October. What is remarkable, however, is that the aggregate earnings growth for the S&P 500 companies was an astounding 42% over the period. Clearly, the stock market was driven by strong profit growth over the period.

It’s also interesting to note some of the major contributors to the earnings growth. Materials companies grew their earnings by 91%, industrials by 79% and financials by 36%. A large contributor to these outstanding numbers is that a low base was used as a starting point for the calculation of the earnings performance of these sectors. However, the base for information technology companies wasn’t very low, and this sector managed to grow its earnings by a buoyant 41%.

Investors loved the operational performance and many of these companies – think Microsoft and Alphabet – got the reward of improved ratings over the period and therefore strong share price performance. The obvious question is what we can expect from these variables – share prices, rating change and earnings – for the next 12 months.

From a macro perspective, it’s very hard to argue for higher P/E multiples – a better rating for US equities – over the next 12 months. First, in our view, the economic growth momentum has peaked, and although we certainly don’t see a recession as a base case, the overall growth rate is likely to slow to well below the 4%+ expected for 2021. Second, inflation concerns and a healthy labour market will ultimately pave the way for an increase in interest rates. These factors, operating in tandem, normally lead to a derating in shares.

Finally, and very importantly, the current rating of the S&P 500 is elevated. The average P/E multiple for the S&P 500 over the past 60 years was 19 times. The current P/E of 28.9 times is 50% more expensive than the long-term average. Some of the higher rating can be explained by the current low policy interest rates. However, this is not sustainable, as argued above.

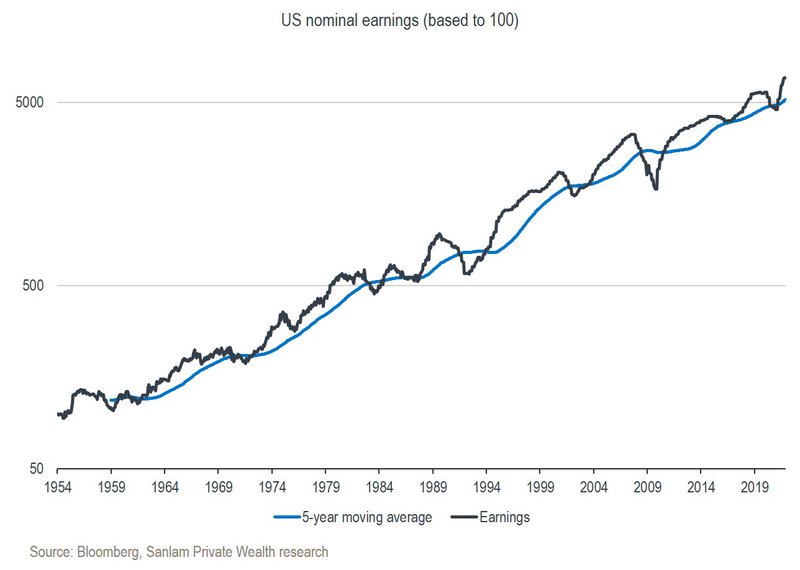

Therefore, for equity price momentum to continue, further good earnings performance from corporate US is needed. As a first step, we should determine whether the current momentum in earnings is sustainable:

It’s clear from this graph that the earnings recovery over the past 12 months has pushed the current earnings base well above the long-term trend line. History suggests that one of two things tends to happen in this scenario. First, the growth trend normally moderates after a spike, and sometimes it can even decline. Second, it would be unrealistic to expect the same momentum in the trend when the base has materially adjusted upwards over the past 12 months.

Finally, if we are correct in our view that the economic growth rate is likely to slow over the next 12 months, it would not be congruent with high growth in company earnings. Just to be clear, we’re not arguing that earnings will be lower. We’re simply suggesting that earnings will grow at a materially lower rate than the 42% recorded over the past 12 months.

A current high P/E rating and expectations of lower earnings growth implies that investors should calibrate their equity performance expectations at levels substantially lower than what was generated over the past 12 months. Given muted performance expectations from global equities and the US equity market in particular, we trimmed our clients’ global equity exposure late in September, favouring non-US equity exposure within the asset class.

Your wealth plan is designed with you in mind. Your financial reality, aspirations and risk profile.

Looking for a customised wealth plan? Leave your details and we’ll be in touch.