Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

Europe:

a continental conundrum

With fears of a possible Marine Le Pen victory in the upcoming French presidential election making headlines almost daily, we take a step back for an objective look at Europe – a region whose economic clout collectively rivals that of the US.

The populist victories of both Brexit in the UK and Donald Trump in the US have lent credibility to the possibility of similar surprises coming out of the continent this year. Currently, most of the excitement is based on the fear that if Marine Le Pen, with her nationalistic and anti-euro stance, wins the election, France could be heading for its own ‘Frexit’.

The likelihood that Le Pen will win the French election is slim, much more so than it was for Brexit or Trump. She has a good chance of making it through the primaries, since the opposition is fragmented across a range of candidates, but in the final round this fragmented support is expected to consolidate behind her opponent. You could well say, ‘but look at what happened with Brexit’. Sure, the polls here could be wrong too, but they would have to be far more wrong for Le Pen to win than they ever were for Brexit.

It does seem ironic that virtually every economist agrees the euro project is fundamentally flawed, yet fears the person who wants to dismantle it. Many economists have questioned the viability of the euro and consider its days numbered. The issue with the euro is that we have very different underlying economies chained to the same exchange rate. Put simply, there is no freely floating currency to act as an escape valve when trouble comes knocking, so any economic stress needs to be addressed through structural changes – not an easy (or quick) solution.

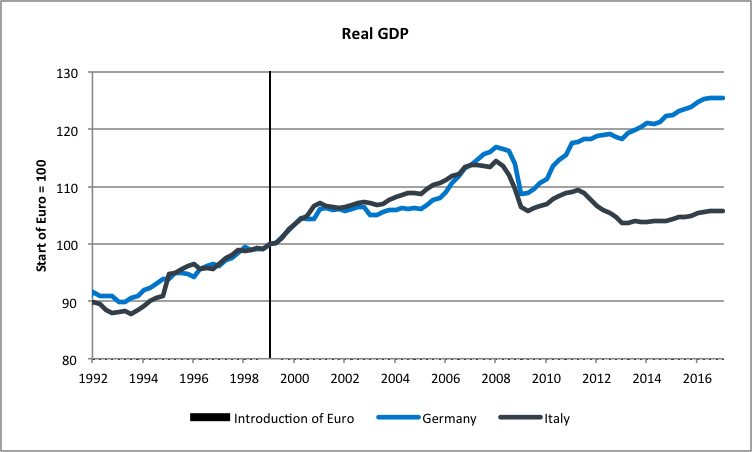

We can see this most starkly in the case of Italy, which hasn’t managed to keep pace with the improvements in productivity that the German economy has achieved. Normally, the lira would have devalued and the deutsche mark would have risen, preserving the Italian economy. Instead, a gross imbalance is making life increasingly tough for Italy while German exports benefit.

CHART 1: German and Italian gross domestic product, adjusted for inflation

If these flaws are so well understood, surely the logical thing would be to admit defeat and abandon monetary union? While we agree that the status quo can’t survive indefinitely and the solution appears obvious, we would caution against betting on the euro’s imminent demise. The euro has widespread public support and politicians consistently affirm their commitment to it, so it’s likely that imbalances have to become larger before they’re more widely addressed.

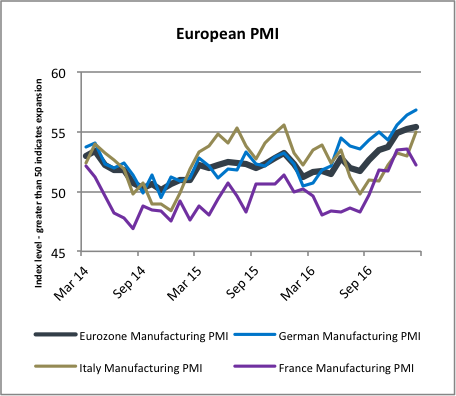

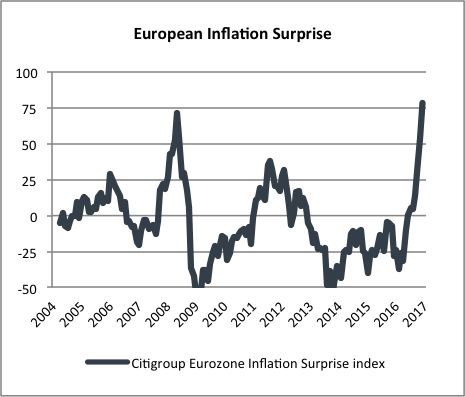

Despite these deep challenges, Europe is signalling some interesting green shoots. Since the fourth quarter of last year, we’ve seen economic data surprising the market with better-than-expected readings. In particular, fears of imminent deflation, a hallmark of the past couple of years, seem much less justified and leading indicators such as purchasing manager readings (PMI) have been gathering momentum across the major economies.

CHART 2 : European economic indicators gathering momentum

CHART 3: European economic indicators gathering momentum

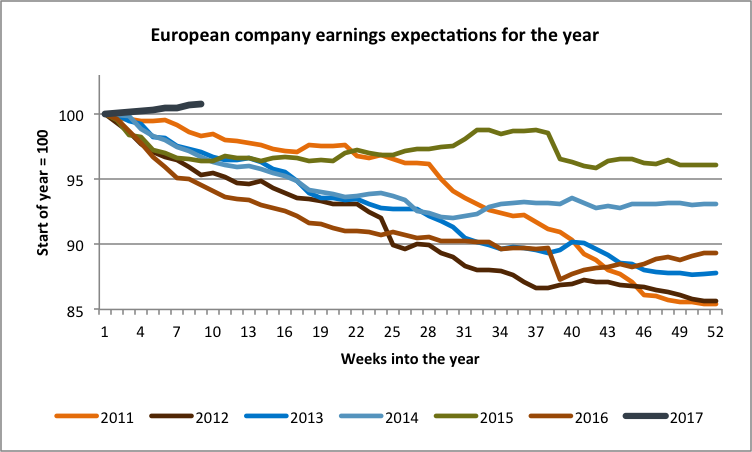

This momentum has filtered through into company earnings. In every year since the recovery from the financial crisis, the market’s expectations for European equity earnings have been lowered as the year went on. While it’s still early days, we’re now seeing the best start to a year in this regard since 2010.

CHART 4: European earnings estimates being revised upwards

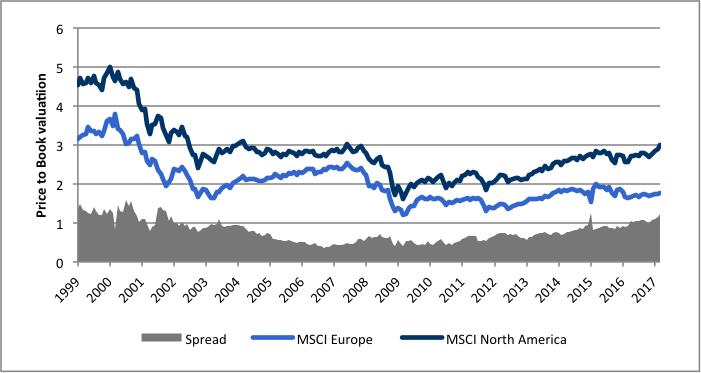

The most important question to answer is: what are asset prices already discounting? In the case of Europe, we’re nervous of the extremely low yields we’re seeing, so we’re not excited about any of the government bonds in the region. However, equity prices are much more reasonable, especially in the context of the elevated levels we see in other global markets.

CHART 5: Europe’s price-to-book ratio relative to US most attractive since tech bubble

In short, while we agree the region faces significant political challenges, we shouldn’t let this blind us to the fact that a part of our investing universe is unloved and offering some value. View this together with the fundamentally improving economic backdrop and we have an interesting investment proposition, albeit not without its risks.

With Article 50 likely to be triggered any day now, we don’t see any end to the Brexit uncertainty. Indeed, Theresa May and her government have had to hold their cards close to their chest to preserve their negotiating position with the European Union, so we don’t actually know much more than we did after the Brexit referendum in June last year. We still think that weakness in the pound is good for the manufacturing sector in the UK, particularly those companies that export their goods. We still think the ever-present uncertainty is not good for business confidence and investment. And we still think that the pound will continue to bear the brunt of the market’s mood swings and remain volatile.

One interesting development is that the UK parliament will vote, in two years’ time, on whether or not to accept the deal that will be negotiated. While this may strengthen UK’s negotiating position in the actual discussions, we believe financial markets will fear that the deal won’t clear this final hurdle and could place a disproportionate emphasis on this possibility.

We constantly challenge the norm. Our investment process is a thorough and diligent one.

Michael York has spent 21 years in Investment Management.

Have a question for Michael?