Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

Europe:

do markets really care about politics?

The impact of politics on financial markets shouldn’t be overstated. This isn’t to say politics doesn’t play a significant role sometimes, particularly in the short term – how else could one explain the dramatic market moves following Brexit, Donald Trump and the French election? It’s just that these occasions are infrequent – when market expectations were wrong and the associated outcome is binary. At SPW, we position our clients’ portfolios conservatively ahead of such events, an approach that has added significant value in the past.

One can’t deny that major events on the political stage do have a marked effect on global markets. In purely financial terms, however, the Brexit vote, for example, is simply about access to the EU economy. The ‘Trump trade’ is about deficit expansion – infrastructure spending and especially tax cuts. The French election only mattered because it could’ve catalysed the euro’s demise.

More often than not political news only dominates the headlines and stirs emotions, but it seldom drives prices of financial assets over the longer term. Tweets, firings, debates and meetings may give clarity on the probabilities of certain outcomes, but their impact on prices should be viewed with scepticism. A great example of this is the weak showing by the Conservative Party in last week’s UK elections. Despite the result taking the market by surprise, the reaction to the news was very benign, with bond yields and equity markets reacting no more severely than they would to any other piece of market news.

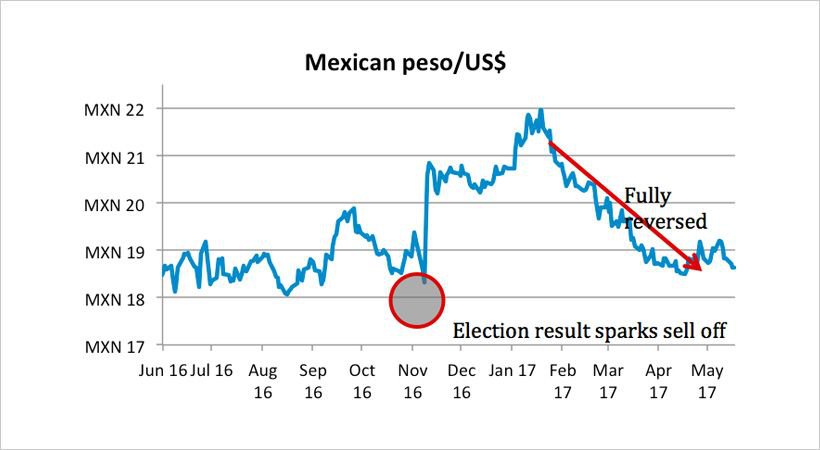

Even in cases where something seemingly dramatic happens, the ultimate effect is usually pretty benign. The ride the Mexican peso has been on since the US presidential election is a case in point. Given all the noise before the election about the border wall, there was a very aggressive move in the peso, weakening after the result became clear from Mex$18 to over Mex$22 to the US dollar – a ~20% move. It may be hard to believe, but this move has completely reversed despite little changing regarding plans for walls and taxes.

Our conservative positioning of our clients’ portfolios in advance of such events – where the result has a binary outcome – stood us in good stead last year when we didn’t anticipate the result of either the EU referendum or the US presidential election. This approach of not overestimating our own forecasting abilities is the foundation of our investment philosophy. We know how difficult it is to forecast events and how correctly anticipating the market’s reaction further compounds the challenge.

We think it’s easier – and better – to focus on companies whose earnings are less dependent on the global outlook. While this may not be the most exciting of strategies, well-managed companies with strong balance sheets and an attractive competitive advantage can offer investors a steady and sustainable way of achieving growth. This is because they’ve traditionally offered higher returns on capital and they have the ability to distribute excess cash to shareholders rather than constantly having to reinvest in their own business.

Quality stocks exist in all sectors (albeit some more than others) and across all geographies. It’s very difficult to predict what the wider theme of the day is going to be and, within our own stock picking, we don’t spend much energy on this risky approach. Rather, we spend our time looking for businesses with these characteristics:

Once we’ve identified the businesses we want to own, we wait for bad news, or a poor quarterly earnings report. This usually spooks the market and gives us a chance to buy a great business at a price where the returns we expect make sense over the longer term.

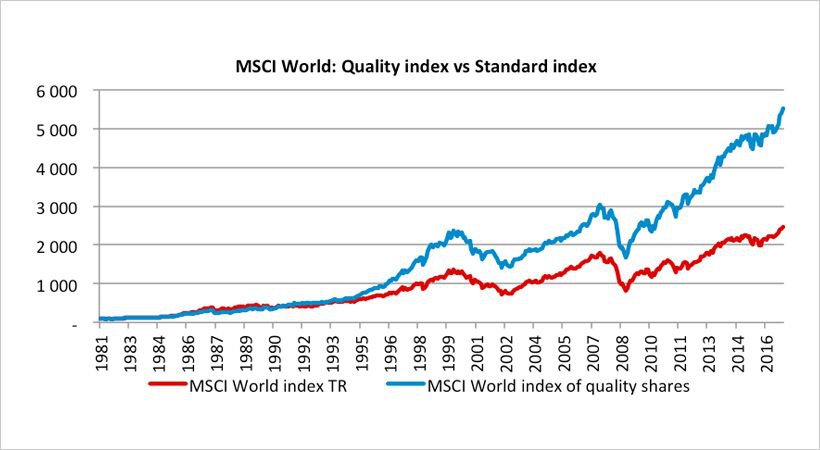

The chart below shows how quality stocks have outperformed the standard index over the past 30 years:

We know quality stocks are not always as fast growing, but because they don’t have upsets nearly as often, their long-term performance has been exceptional. Of course their share price can fall like any other stock, and their earnings will suffer if the economy is suffering, but the underlying businesses are more resilient and they usually bounce back very quickly once confidence returns. In times of political uncertainty this approach can offer some peace of mind.

We can help you maximise your returns through an integrated investment plan tailor-made for you.

Niel Laubscher has spent 10 years in Investment Management.

Have a question for Niel?