Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

GOLD: WHAT'S DRIVING

THE PRICE SURGE?

The gold price recently reached a new all-time high in US dollar terms, breaking through the US$2 000 per ounce psychological level. What’s remarkable, though, is that the global interest rate environment is not at all supportive of the current high price. Something else is driving the demand for the precious yellow metal. Is this sustainable, or is it just short-term speculation?

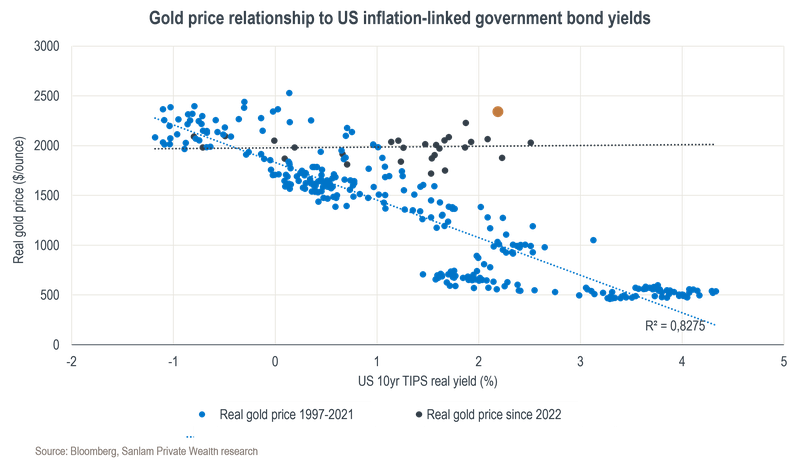

Gold has historically traded in an inverse relationship to real (inflation-adjusted) interest rates. The rationale for this is that gold is used as a store of value (it protects against inflation). However, it pays no income, so instead of owning gold as a safe-haven asset, an investor can buy an inflation-linked government bond that would provide the same benefit as gold, but also an income stream. The higher the real interest rate on these bonds, the less appealing gold becomes with its zero yield, and vice versa.

The chart below shows the tight historic relationship between the gold price and the yield on a 10-year US Treasury Inflation-Protected Security (TIPS) before 2022. At the current TIPS real yield of 2.2%, one would expect a gold price of closer to US$1 200 – almost half the current spot gold price!

However, it’s clear that since 2022 – when Russia invaded Ukraine – the gold price has disconnected from real interest rates in the US. Historically, this has happened when central banks have changed their buying or selling patterns of gold reserves, or when geopolitical tension or financial risk events have driven safe-haven demand for gold.

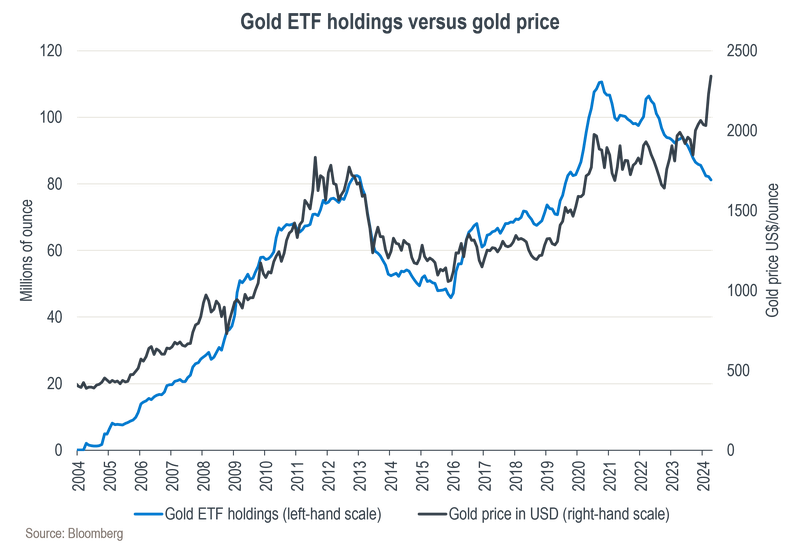

At present, the strong demand for gold seems to be coming from the East, while Western demand is muted given the high interest rates on offer. The chart below shows that gold holdings by exchange-traded funds (ETFs) have been declining in North America and Europe since 2022. Historically, the gold price has correlated highly with gold ETF holdings, which makes the recent rally in the gold price seem out of place.

However, the decline in Western demand for gold has been more than offset by physical buying by central banks and private investors in the East. Following the freeze on Russian foreign exchange reserves after its invasion of Ukraine, central banks of countries like China, Russia and Turkey have increased their purchases of gold to insulate themselves against the risk of foreign sanctions in the future. Despite China’s central bank having the seventh largest gold holdings in reserve, gold is still only around 5% of its total reserves versus 15% on average globally – so the buying trend may yet have some runway left.

Furthermore, with Chinese investors being scarred by poor equity returns and a severe downturn in the property market, demand for gold has risen sharply over the past few months. The Chinese market has historically exhibited strong momentum behaviour, which is likely to contribute to wilder price movements in the gold price.

Nothing breeds FOMO (fear of missing out) more than rising prices, and we’ve noted that net long positioning of gold futures has risen sharply in the last two months. Gold ETF holdings in the US have also recently turned positive.

With the gold price showing signs of speculative buying and having disconnected from its interest rate drivers, one should perhaps approach gold with more caution in the near term. However, we do believe that the floor price for the metal has moved materially higher in recent years and should continue to find support from the shifts in the geopolitical landscape and rising fiscal risks threatening the prospects for traditional safe-haven government bonds.

In addition, a pivot towards lower interest rates in the West is likely to be supportive of gold. From this perspective, investors would be wise to maintain exposure to the yellow metal as a valuable hedge in a diversified portfolio.

We can help you maximise your returns through an integrated investment plan tailor-made for you.

Niel Laubscher has spent 10 years in Investment Management.

Have a question for Niel?