Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

How to build a

robust portfolio

Investment managers often construct their clients’ portfolios with a dominant macro view – and associated expectations of the future – dictating their decisions. In today’s uncertain investment environment, however, we believe it’s impossible to forecast outcomes with any degree of conviction. It’s therefore crucial that – guided first and foremost by valuation – portfolios are crafted for robustness and resilience across multiple scenarios.

‘Events such as the 9/11 attacks, 2009 global financial crisis, Arab Spring, Brexit, and election of Donald Trump continue to prove that traditional forecasting methods leave decision-makers dangerously exposed to unanticipated events.’

These are the words of Frans Cronje of the South African Institute of Race Relations, and we couldn’t agree more. Decision-makers, including investment managers, who claim they can forecast with conviction in today’s uncertain macro environment are, to put it bluntly, either very brave or very stupid. But this, unfortunately, is what many are still doing – crafting both equity-only and multi-asset client portfolios guided by a particular macro ‘story’ or outlook and associated expected outcomes.

When you position a portfolio based on one-dimensional future expectations, you may of course get it right and achieve excessive investment returns. However, you can also get it horribly wrong. And the pendulum may have a very short swing – a case in point is the outcome of the recent ANC leadership election, in which Cyril Ramaphosa pipped Nkosazana Dlamini-Zuma to the post by an extremely tight margin. It was a close call from the start, but people were prepared to ‘invest’ with conviction based on their view of who would win. The outcome being binary, however, they could just as easily have got it wrong.

At Sanlam Private Wealth, we take a different approach to constructing our clients’ portfolios. Our investment methodology first involves a bottom-up process, where each asset is assessed on individual merit. This is based largely on expected return – a function of both the value as well as the ‘story’ associated with the company in question.

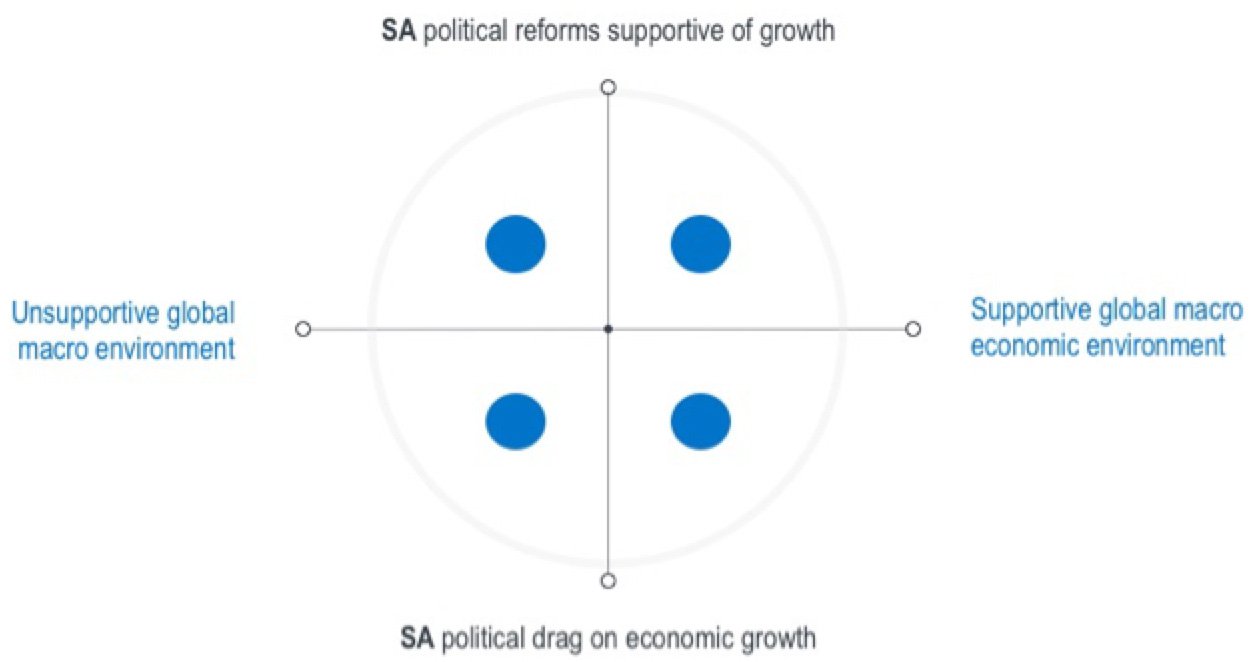

From a macro perspective, we divide the investment landscape into four quadrants, each defined by a combination of particular global and local economic cycles – the local cycles often dominated by the prevailing level of political certainty:

Different asset classes and even equities will generally behave differently in each of the four scenarios or phases of the economic cycle. In the bottom left quadrant, both local and global economic activity is under pressure – shares that tend to perform well here are defensive in nature and from a South African perspective, they are rand hedges, such as liquor and tobacco shares (economic cycles don’t appear to have an impact on whether or not people smoke). Where the global environment is supportive, but there’s uncertainty in the local economy (bottom right), commodity prices are likely to appreciate and our mining shares tend to do well.

If both the global and South African stories are positive (top right), cyclical shares are likely to outperform. Apart from the usual suspects, one would expect banks and even construction counters to do well here. In the top left quadrant, it’s clear that the focus should be on local exposure – domestic defensive shares that will benefit from local economic growth.

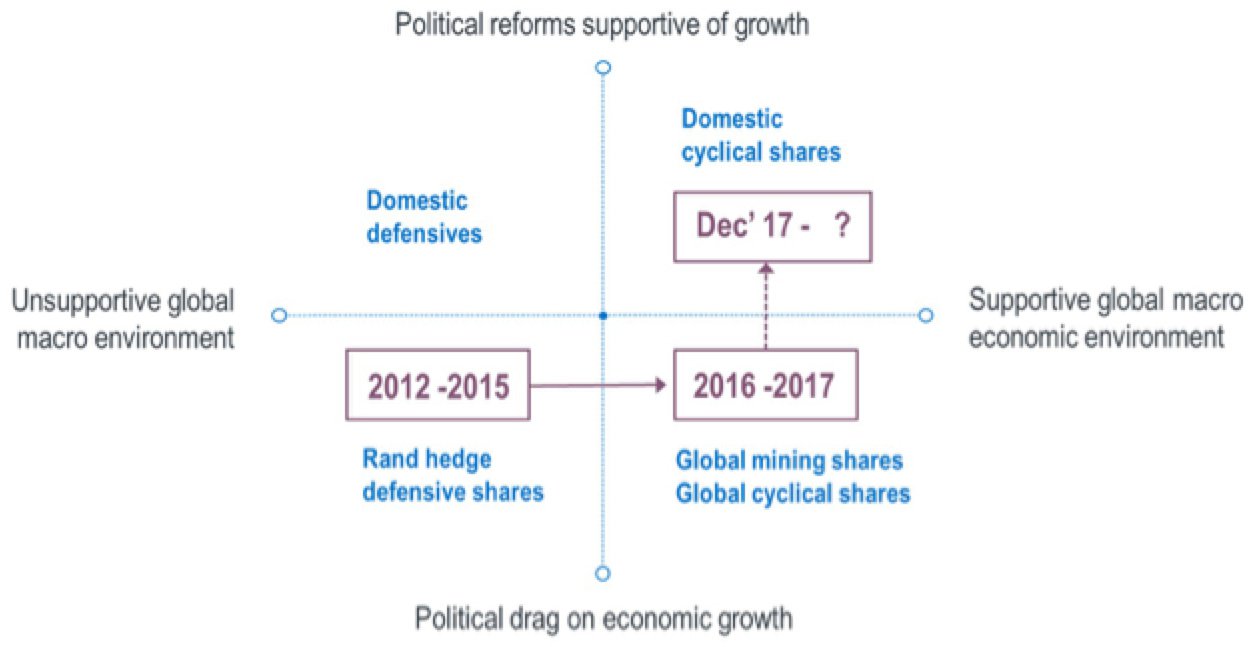

It’s important to note that there’s normally a logical, sequential flow between the four quadrants. The diagram below shows the current position of our investment environment:

From 2012 to 2015, we had a rather pedestrian recovery in global economic growth, but from 2016 to 2017, it shifted gear to a synchronised recovery. Investors were still highly uncertain about local prospects, however, and our growth rate reflected this. In 2018, we should start seeing an uplift in the South African economy. So while we’re currently still mainly in the bottom right quadrant, we could soon be moving to the top right scenario.

If we map the main shares in SPW’s house view equity portfolio on our four-scenario diagram, the picture looks like this:

The tilt of the portfolio lies in the two right quadrants – to benefit mainly from global growth, but also from a potential recovery in the local economy.

There is one proviso to benefiting from investing according to an investment landscape model such as this: you have to be early. Since the market tends to lag, it’s crucial to find the right assets before the cycle moves into the quadrant with which they’re associated. The cycle will then of course continue and the focus will shift to other shares that will benefit from the particular macro overlay at that time.

The implication of this is of course active asset management, taking profits when the good news is already reflected in the share price, and looking for assets whose price doesn’t yet reflect their potentially better prospects. So despite the fact that a particular share may be in the ‘correct’ quadrant at a certain time, it may already be priced in for that environment. If it becomes too popular or expensive, we’ll sell off and move to shares in the next quadrant if we know the cycle is changing.

On the other hand, when the cycle migrates, some of the assets in the ‘original’ quadrant may suddenly become very cheap. In this case, we’ll be guided by valuation as well as cycle shifts in deciding whether to pursue these opportunities.

Despite the fact that economic and market cycles may be ‘normal’, and many assume it’s easy to forecast the sequence of events, it’s not quite so simple. First, although events are more often than not sequential, the time spent in each phase will vary from cycle to cycle. In short, although the quadrant model is a handy tool, it does have shortcomings in terms of timing – deciding when to amend a portfolio. Second, we know that human intervention in the financial cycle always opens it up for surprises and of course, shocks. For these reasons we warn against a one-dimensional strategy.

At SPW we’ll always construct portfolios to be robust and resilient across multiple scenarios. While we tend to have a bias in a particular quadrant, our clients’ portfolios will also contain shares in the other quadrants. Besides the price considerations mentioned above, this is to ensure balance, and importantly, to reduce exposure to risk for our clients.

Diversification across the various scenarios is in our view the most effective way of ensuring our clients’ portfolios outperform over time – an approach that has borne fruit over the past 10 years. It will remain part of our tried and tested investment philosophy and process in protecting and growing our clients’ wealth.

Your wealth plan is designed with you in mind. Your financial reality, aspirations and risk profile.

Carl Schoeman has spent 22 years in Investment Management.

Have a question for Carl?