Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

LOADSHEDDING: IMPACT

ON YOUR PORTFOLIO

Recent company results have started to expose in numerical terms what most investors have understood but struggled to quantify: loadshedding is having a significant impact on the profits of companies with South African operations. Armed with improved information provided by these businesses, we examine the implications for our clients’ portfolios.

First, it’s important to note that a major proportion of the value in JSE-listed companies lies in operations outside South Africa. There are multiple ways to slice and dice the available data, but our analysis suggests that ~54% of the value of the FTSE/JSE All Share Index (our benchmark for South African-focused portfolios) is outside the country, while around 41% of the value of the FTSE/JSE Shareholder Weighted All Share Index (SWIX – the benchmark for many of our peers) lies beyond our borders.

Second, we remind readers that most of our mandates at Sanlam Private Wealth hold a proportion of offshore assets. So these portfolios are obviously less impacted by loadshedding. For the purposes of this article, we’ll focus on the local market, but for most of our clients, the numbers highlighted below can be downscaled by the proportion of assets held outside South Africa.

How has loadshedding impacted local businesses? Although it has become materially worse over the past six months or so, the concept has been with us for a number of years and businesses have adapted to be able to handle occasional power cuts to some extent. So with the increase in the intensity of loadshedding over the past few months, companies have generally been able to make a plan. The problem is that the higher levels of loadshedding translate into increased costs.

Loadshedding affects the companies listed on the JSE in a number of ways. The most direct impact is typically felt by businesses that require electricity for the creation of products, including manufacturers, miners and telecom operators. If their operations are disrupted by loadshedding, these businesses will have less product to sell. Miners usually have agreements with Eskom for load curtailment rather than loadshedding, but they are also affected, particularly in the area of platinum smelting.

Larger manufacturers are typically located at national key points, where they are immune from loadshedding, but this isn’t always the case for smaller players. Cell phone operators, which have thousands of towers all over the country, don’t have the same protection and must rely on a combination of batteries and diesel generation. In general, capital-intensive businesses like these have wider profit margins, so the incremental costs don’t impact a particularly large proportion of profits.

The next group of businesses that suffer are retailers. While these companies don’t make their own products, they need electricity to be able to sell them. Food and grocery retailers need electricity not only to keep the lights on and the credit card machines working, but the fridges and bakeries also consume a lot of power.

Grocers typically have thin margins. Shoprite, the most profitable of the South African grocers, had an operating profit margin after leases of only 4.3% in the year to June 2022. So the additional impact of running generators hurts. Shoprite’s six-month results to December 2022 indicated the trading margin had fallen despite excellent revenue growth.

Finally, service businesses experience the least pain. While it costs a lot to keep offices illuminated, this expenditure is relatively small compared to the ‘people’ costs of running a bank or insurer.

Businesses with customers within South Africa will also feel the pain of slower local economic growth resulting from the impact of loadshedding on the wider economy. This means we can expect slightly lower growth over the coming years than would have been the case without the high levels of loadshedding.

Investors should also be aware of loadshedding’s implications for capital allocation. All the management teams of companies impacted by loadshedding that we’ve spoken to are looking at options to generate more of their own power. The telecom companies, for example, are spending billions of rands on batteries and generators for their towers. Many businesses are installing solar panels on rooftops, while several miners are involved in larger-scale solar projects. However, spending this capital on solving electricity problems means less is available for other growth initiatives.

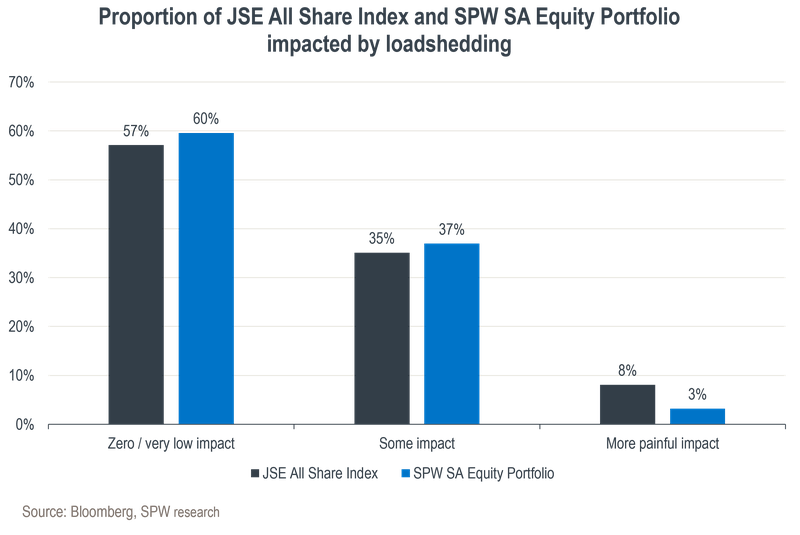

What are the implications for our clients’ investment portfolios? The graph below illustrates the exposure to loadshedding within Sanlam Private Wealth’s South African equity portfolio compared to the wider local market. The ‘zero/low impact’ block includes companies like Richemont, Naspers, Bidcorp, British American Tobacco and BHP, where most of the value sits offshore. In the second group we find companies such as FirstRand, MTN, Sanlam, Bidvest and Pepkor that are impacted by the slower general economy, but whose direct costs are not too painful in the context of overall profits. The third batch contains businesses where the impact is most keenly felt, like the platinum miners, Pick n Pay, Vodacom and Tiger Brands.

As the chart shows, Sanlam Private Wealth’s South African equity portfolio has a greater proportion of its holdings in businesses with zero or very low impact from loadshedding, and most importantly, materially less exposure to those businesses where the impact is most painful. Our client portfolios are thus relatively less affected by loadshedding than the wider market.

While the above analysis shows which businesses are affected more than others, it doesn’t show how much of the good or bad news has already been baked into prices. It should be remembered that the price one pays for an asset is a key determinant of whether that asset delivers market-beating returns or not.

We believe our current portfolio positioning has protected our clients from the worst impacts of loadshedding. However, we remain vigilant for opportunities where the market might be pricing in a worse scenario than what actually plays out.

When formulating your investment strategy, we focus on your specific needs, life stage and risk appetite.

Looking for a customised wealth plan? Leave your details and we’ll be in touch.