Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

SURVIVING THE

DIVIDEND DROUGHT

This year is likely to be challenging for income investors – the economic impact of COVID-19 has compelled many JSE-listed companies to suspend dividends to ensure they don’t run into financial difficulty. In our view, the best strategy for investors is to try and tighten the belt from an income point of view over the short term – and ride out the dividend drought. Once the pandemic is finally behind us and the world returns to some semblance of normality, most companies should resume dividend payouts.

Read more below or listen to Renier's views here:

‘Cash is king’ is a popular phrase describing the preference of businesses and investors for cash. Cash flow is the lifeblood of every business – it provides liquidity to investors and is straightforward in terms of value (R100 in cash is simply worth R100).

Dividends are the excess cash that businesses can distribute to their shareholders after meeting their ongoing business cash flow requirements. They are therefore a good indicator of a business’s power to generate free cash flow, provided it is retaining adequate funding to meet future business needs.

For dividend-focused investors, assessing the sustainability of a company’s dividend payments is crucial – a high dividend yield in itself may potentially signal the market’s concern over the ability of the business to grow its dividends in future. We’ve seen cases in our local market where listed companies ‘over-distributed’ dividends, which eventually contributed to a strained balance sheet when they went through a difficult period. Examples include African Bank (ABIL), Anheuser Busch and a number of listed property shares.

Interestingly, an investor who purchased ABIL at the start of 2005 for R13.66 would have received a total of R15.37 in dividends per share – more than the original investment – by 2013, before the bank collapsed in 2014. If ABIL had a more conservative approach to accounting for bad debts (as Capitec did), resulting in less generous dividends, the story might have played out differently.

Many investors prefer high-dividend-paying shares in order to receive an income without having to sell shares for this purpose. At Sanlam Private Wealth, we prefer to have a total return focus (valuing capital growth and income equally) when we construct share portfolios, for these reasons:

Companies that can reinvest capital into their businesses at a higher rate of return than the general market is likely to provide for investors, should do so, rather than distribute dividends. Those with more muted (or speculative) prospects with regard to available capital should rather return the cash to shareholders. This probably applies to most companies, as only a few have demonstrated that they can consistently reinvest their capital at high returns. Many more have failed through new ventures or acquisitions that have fallen short of expectations.

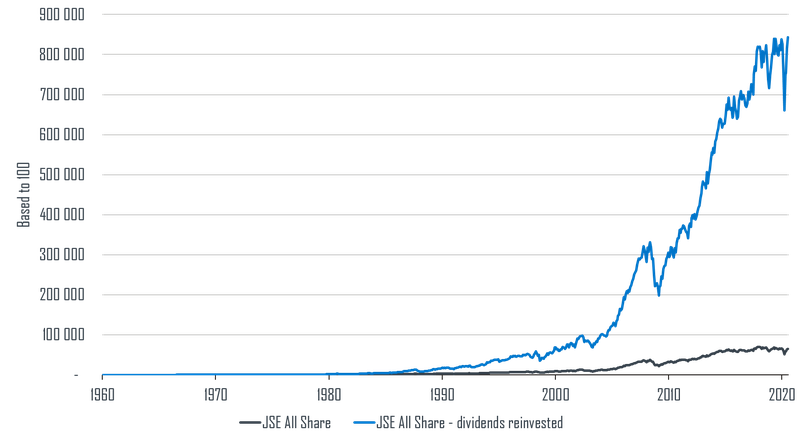

Over the long term, dividends (if reinvested) contribute meaningfully to an investor’s total return. The chart below shows the performance of the FTSE/JSE All Share Index with and without dividends since 1960:

The impact of dividends reinvested

Source: Iress, SPW Research

This year is likely to be particularly difficult for dividend income investors, as the economic impact of the pandemic has forced many companies to put dividend payments on hold in order to preserve their balance sheets. Even stalwart South African dividend payers such as banks and insurance companies will have to skip dividend payments under advice of the Regulator.

While this may be disappointing for investors who hold these shares for their dividends, we view this as a prudent move to strengthen balance sheets until the world returns to normal. A bankrupt company can’t return to paying dividends in the future, while cash that is retained for now will stay on the balance sheet and can always be distributed later.

To add to the woes of income investors – while borrowers are celebrating the 300 basis point cut in the prime rate so far this year, it will come at the expense of the interest rates that savers will earn on their bank and money market deposits. The prices of many of the dividend shares have also come under pressure, which could have a negative long-term impact on an investor’s capital base should they sell some of these shares at these levels to supplement income.

In our view, the most appropriate strategy at this stage would be for investors to try and economise as much as is feasible from an income point of view over the next few months, and ride out the dividend drought until companies reinstate dividends once the COVID-19 pandemic is a thing of the past. The lower interest rates on savings also increase the relative attractiveness of South African dividend-paying shares, especially at their current depressed prices.

In our Dividend Income portfolio, we invest in companies with above-average dividend yields, but also with the ability to sustainably grow these dividends ahead of inflation over time. While the next year’s yield may be impacted by a few companies deferring dividends, the expected dividend income yield on the portfolio is around 7% for the year thereafter. This remains an attractive return relative to money market rates, even before the prospective capital growth and the more favourable tax treatment for high marginal tax rate investors are taken into account.

When formulating your investment strategy, we focus on your specific needs, life stage and risk appetite.

Looking for a customised wealth plan? Leave your details and we’ll be in touch.