Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

TWO-SPEED GLOBAL MARKETS:

SHOULD WE BE DANCING NEAR THE DOOR?

This year has seen the rise of two-speed global markets as a direct result of the ‘Great Lockdown’, with the performance of mainly tech stocks on the one hand, and ‘old economy’ shares on the other, diverging widely. What are investors to make of this highly unusual investment landscape? It has attracted a throng of momentum followers eager to chase the market trends. At Sanlam Private Wealth, we remain committed to our philosophy that valuation will trump fashion over the investment cycle – in our view, while we can certainly enjoy the party, it’s best to dance near the door in the present circumstances.

Read more below or listen to David's views here:

Since the world went into lockdown in March, global markets, especially those in the US, have been marching to the beat of two very different drums. Businesses whose operations have benefited from COVID-19 lockdowns – such as technology companies – have been rewarded handsomely as people spend more money online and businesses migrate to cloud computing. At the same time, old-economy stocks have struggled.

The S&P 500 has recorded 12 new all-time highs since the March market crash and despite the global economy now being distinctly worse off than it was then, it’s now trading at 1% above its high in February (5% year-to-date).

The six largest tech stocks in the S&P 500 now account for almost a quarter of the index, more than financials, energy and industrials combined. These shares have performed excellently so far this year: Apple is up 58%, Amazon +71%, Netflix +53%, Facebook +33%, Microsoft +33% and Google parent Alphabet +15%. Excluding these tech heavyweights, however, the S&P 500 is down year-to-date. The performance of old-economy market stalwarts like Goldman Sachs (-12%), 3M (-3%), Coca Cola (-5%) and United Health (+6%) illustrate the market’s divergence.

The valuations of these mega-cap tech companies are looking stretched, however, with Amazon trading at 56 times its expected earnings for the next 12 months (forward price-earnings, or P/E) and Netflix at 57 times. While Apple and Microsoft are less exorbitant at ~31 times, this is still almost a 50% premium to the 22 times that the S&P 500 as a whole is trading at.

At a time when visibility around the global economy is murky, tech stocks do provide higher levels of clarity over both the short term and a few years out. Despite a not-unexpected correction over the past couple of weeks, markets are clearly willing to pay up for this, as well as for these companies’ strong cash generation and healthy balance sheets. But no matter how predictable the profits of a business are, it’s only ever a good investment if you buy it at an appropriate price.

To help the economy deal with the pandemic and resultant job losses (11 million fewer people are employed in the US today than in February), global central banks have provided extraordinary levels of monetary stimulus in the form of low interest rates. They’ve made it clear to markets that rates are likely to stay low for some years to come.

Low bond yields mean that investors are searching for yield away from bonds, which also lowers the required return for equities. A one percentage point change in the discount rate for developed market equities translates to a roughly 12% change in the value of those equities, all else being equal. US bond yields are down about one percentage point since February, so the rise in the S&P 500 would be reasonable if it weren’t for the fact that global GDP has taken a major hit – which will undoubtedly drag down aggregate corporate profits.

Many ideas have been put forward as reasons for the divergence. One of the simplest is that for growth companies, a greater percentage of their current value lies in earnings that will be generated beyond five years into the future. This means that their valuations are more sensitive to changes in interest rates.

The key reason for the rise in tech stock prices is that these companies are growing revenue and profits throughout the pandemic, while others are struggling. And despite the rout this month, this doesn’t seem like a temporary phenomenon, but rather an acceleration of the longer-term trend towards digital. In effect, the COVID-19 pandemic has brought the earnings streams of key tech companies forward by a few years, but it has pushed those of non-tech companies out by two years.

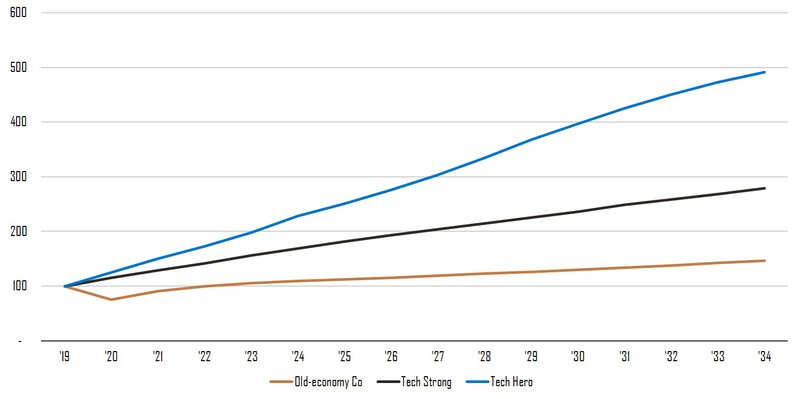

In the chart below, we consider three generic companies with different earnings growth paths. The typical ‘old economy’ company will likely only return to 2019 profit levels in 2022, by which time the ‘strong tech’ company will have increased its earnings by ~40% above 2019 levels, and the ‘tech hero’ will have increased earnings by ~70% from 2019 levels. The key difference is that while normal company earnings are declining in 2020, tech earnings continue to power ahead.

Earnings profiles for 3 representative companies (based to 100 in 2019)

Source: SPW research

If these companies all have the same risk profile, all grow at the same rate after 2034 and we use the current low interest rates, they should trade at forward P/E multiples of 20 times (old economy), 24 times (tech strong) and 34 times (tech hero). Note, however, that the forward earnings for the old-economy company are below trend, making the P/E appear higher. Nevertheless, the key takeaway is that even assuming low interest rates for years to come, the market is pricing in particularly high and sustained growth rates for the mega-cap tech companies. Not only do such growth rates appear optimistic, but it seems imprudent to pay for the next 15 years of growth in such an unpredictable world.

Another driver of the optimistic valuations is that the current stock market rally has attracted many small US retail investors, who typically trade with high frequency and tend to be momentum followers. Their purchases of high-flying stocks like Tesla serve to fuel further momentum and attract new punters. History has been unkind to such momentum chasers, as evidenced by the dot-com bust in 2000.

This time around, however, the tech winners are generating substantial free cash flow and have built attractive moats around their businesses. With regard to the near-monopoly status of these companies due to network effects, there are two competing views. As we’ve written previously, network effects are the most sustainable competitive advantage (the more people on your network, the more attractive it is for others to join) and can justify both higher growth expectations and lower risk. However, monopolies also attract regulatory scrutiny, which has been building around the world.

So what are investors to make of our two-speed global markets? While optimism appears to continue unabated among some smaller momentum followers, large, professional investors are displaying more caution, as evidenced by the recent rise in the VIX (an index that’s a popular measure of implied volatility, also known as the ‘fear gauge’). They may be enjoying the party, but they’re certainly dancing near the door.

In our global portfolios, we’ve remained true to our philosophy and trimmed some of our more expensive tech exposure of late, switching the cash into some less-fashionable names that are trading at more attractive valuations. While only time will tell whether we’ve timed this correctly, we maintain our view that over the investment cycle, valuation will trump fashion.

Using your equity portfolio to secure credit allows you fast access to capital.

Looking for a customised wealth plan? Leave your details and we’ll be in touch.