Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

The value of hedge funds

in a multi-asset portfolio

Alternative investment instruments such as hedge funds have often been avoided by traditional investors who may not be aware of the opportunities they present to better protect invested capital as part of a robust portfolio. At Sanlam Private Wealth we offer hedge funds in our multi-asset solution, to ensure our clients’ portfolios are well diversified and positioned to generate returns in both normal and extreme market conditions.

The importance of a well-diversified investment portfolio to protect against market risk cannot be overemphasised. But even though a diversified equity portfolio can eliminate company and sector-specific risks, it may still be heavily exposed to the market’s general direction. The inclusion of bonds, with returns largely uncorrelated to equities, has become a common way to protect the capital of investors who may not want full exposure to equity risks. Apart from a small allocation to cash, this is the extent to which the traditional investor tends to diversify their portfolio.

A world of investment opportunity remains untouched by these investors. Hedge funds (essentially pooled funds that use derivatives and apply various strategies to generate uncorrelated returns to equities), private equity and agricultural commodities are but a handful of the investable instruments presented as alternatives, due to their returns being largely independent of traditional financial markets.

Why then have traditional investors been reluctant to invest in these instruments? Primarily because alternative investments often require large initial investments, or because the nature of the markets in which they trade are either illiquid or unregulated. As a result, many have come to see alternative investments as a luxury enjoyed by only an elite few.

South Africa’s first hedge fund was launched in 1998 with many more following, but recent years have seen major changes in the industry. With hedge funds now regulated under the Collective Investment Schemes Control Act (CISCA), a wider set of investors can enjoy access to these alternatives in a well-regulated, liquid environment. The returns of a carefully selected set of hedge funds can be largely uncorrelated to traditional asset classes under stress. This means an investment in a fund of hedge funds diversifies exposure across a number of expertly selected hedge funds, and is able to be both a diversifying and return-generating component in an investor’s portfolio.

When selecting a diversifying asset as part of a more sophisticated approach, one should naturally consider its ability to add value in both normal and extreme market conditions. In doing so, it is of utmost importance to consider the cost – noting that this doesn’t only mean the sum of fees paid, but also the return sacrificed under normal conditions to cater for the extreme. In other words, cost is the difference between the diversifying asset’s after-fee return and the return of the asset against which protection is typically sought.

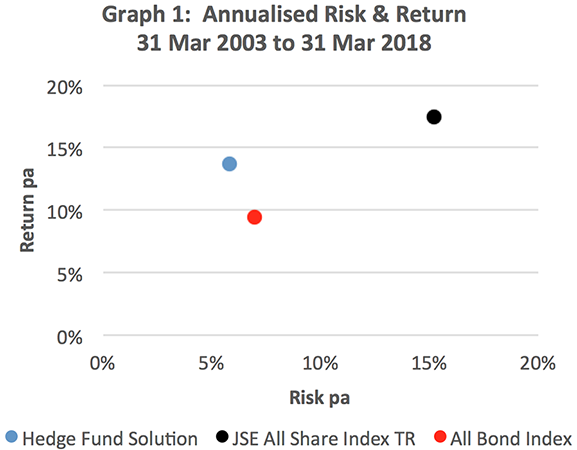

Graph 1 considers the longer term, annualised risk and return characteristics of equity, bonds and a hedge fund solution* over the past 15 years. The farther left the asset finds itself on the graph, the lower its volatility, and the higher up it is, the better its return.

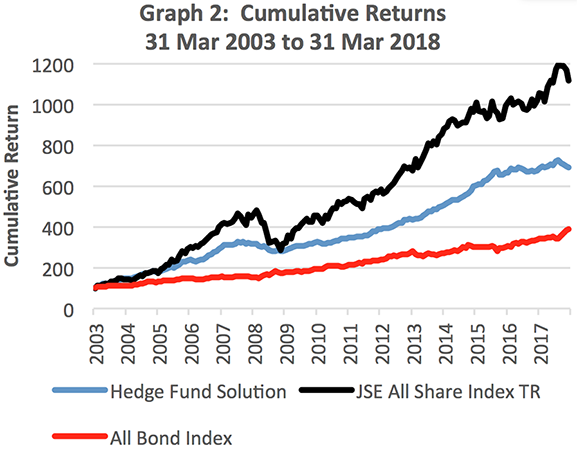

The significantly lower volatility of the hedge fund solution and bonds in comparison to equity indicates that their inclusion in a portfolio reduces risk. Also, at a lower volatility than bonds, the hedge fund solution generated an annualised return of 13.73% (after all fees), while bonds returned 9.48%. This effectively means that in terms of returns sacrificed, the hedge fund solution was a considerably less costly diversifying asset. The cumulative effect over the 15 years is shown in Graph 2.

* The performance used for the hedge fund solution in this analysis is after all fees and represents the actual fund of hedge fund track record of the portfolio manager at THINK.CAPITAL.

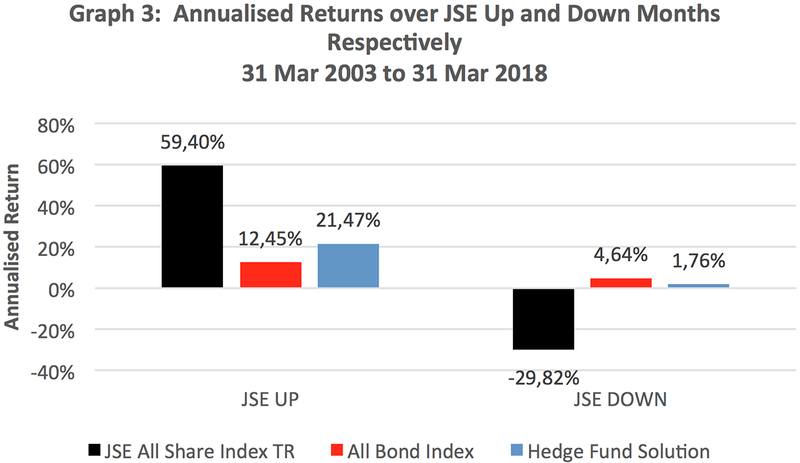

To consider the diversification during extreme periods, bonds and the hedge fund solution returns are viewed over all equity up-market months separately from all the months in which the JSE incurred a loss. Graph 3 shows that the hedge fund solution’s outperformance of bonds was due to more effective participation in upmarket months (returning 21.47% per year), while exhibiting fairly similar positive returns when equities were down (1.76% per year).

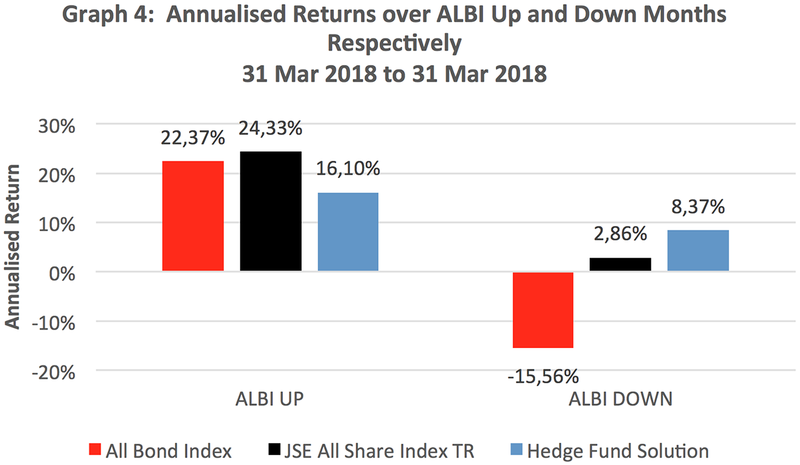

The hedge fund solution should not simply be seen as a substitute for bonds, however. In a similar analysis, this time separating bond up-months and down-months, Graph 4 shows the hedge fund solution’s returns as largely uncorrelated to bond returns over extreme periods. An annualised return of 8.37% was generated by hedge funds over all All Bond Index (ALBI) down-months.

The complementary nature of hedge funds to both equity and bonds creates an opportunity to construct a robust portfolio to better protect invested capital, with the potential of generating returns in line with equity over time. At Sanlam Private Wealth we’ve included hedge funds in our multi-asset solution, providing our clients with access to additional sources of return to meet each client’s specific needs.

Elmien Wagenaar, Investment Manager and Director of THINK.CAPITAL, contributed to this article.

We constantly challenge the norm. Our investment process is a thorough and diligent one.

Michael York has spent 21 years in Investment Management.

Have a question for Michael?