The share price of Impala Platinum – the second largest platinum producer in the world – reflects a company and industry that is not expected to earn sustainable returns on capital. We don’t agree with the market’s view, and anticipate the share will outperform the market.

The reasons we believe the stock will outperform over the coming years are:

- Electric cars that use electric motors instead of internal combustion engines for propulsion comprise less than 1% of all vehicles cumulatively, but we expect exponential growth in this market. France recently announced plans to end the sale of petrol and diesel cars by 2040, and Volvo has said all its cars will be electric or hybrid from 2019. However, we believe the impact of this on platinum-group metals (PGMs) is overplayed – the writing is not yet on the wall for internal combustion engines. We can’t know for certain when, or even if, electric cars will overtake them in future.

- A large proportion of PGM production is unprofitable. We therefore expect further restructuring and consolidation, which will swing the demand/supply balance and consequently the price of PGMs. It’s of course impossible to predict a time frame, so if the rewards outweigh the risks – which in our view, they do – we believe it’s correct to purchase the share regardless of the levels of discomfort.

- Impala Platinum can weather a further downturn if it occurs. The company’s balance sheet carries minimal net debt. Impala Platinum isn’t the weakest link in the industry, so a further downturn will likely lead to other producers removing supply from the industry, which will have a positive impact on PGM pricing. This will be uncomfortable in the short term, but importantly provides some capital protection.

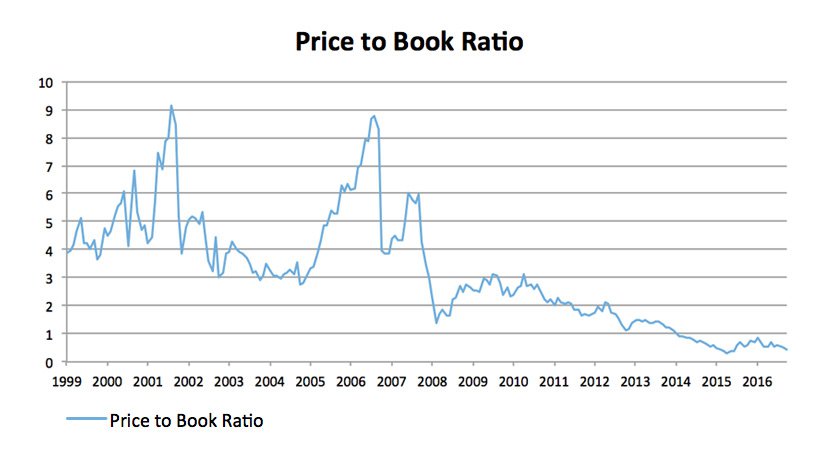

- The Impala Platinum share is flirting with 20-year lows on a relative basis to the market:

- The increase in production over the next three years from the Impala lease area means there will be greater scale, which is vital to mining, and as a consequence we expect better margins and returns to investors.

In the words of American investor and writer Howard Marks, ‘It’s not what you buy; it’s what you pay for it.’