Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

Impala Platinum:

still set to outperform

The share price of Impala Platinum, the second-largest platinum producer in the world, reflects a company and industry struggling to keep head above water. We invested in the company last year, as we disagreed with the market’s assessment on its valuation and anticipated that the share would outperform over the longer term from a low base. A year later, the share has lost further ground against the market. We still believe our investment thesis makes sense – but patience is required to see it unfold.

In July last year, we made the case for Impala Platinum, and we’re still positive about the share. Here’s why:

The hype around electric vehicles as a replacement for internal combustion engine vehicles is gaining traction. Although we agree with the market that the number of electric vehicles is set to grow exponentially (it’s currently less than 1% of the total vehicle market), we believe the effect of this on platinum group metals (PGMs) is overplayed. In our view, gasoline vehicles will continue to play an important role. Also, we expect that hybrid vehicles (a mix between electric and internal combustion engines), which still require a catalytic converter, will also play a vital role in the foreseeable future.

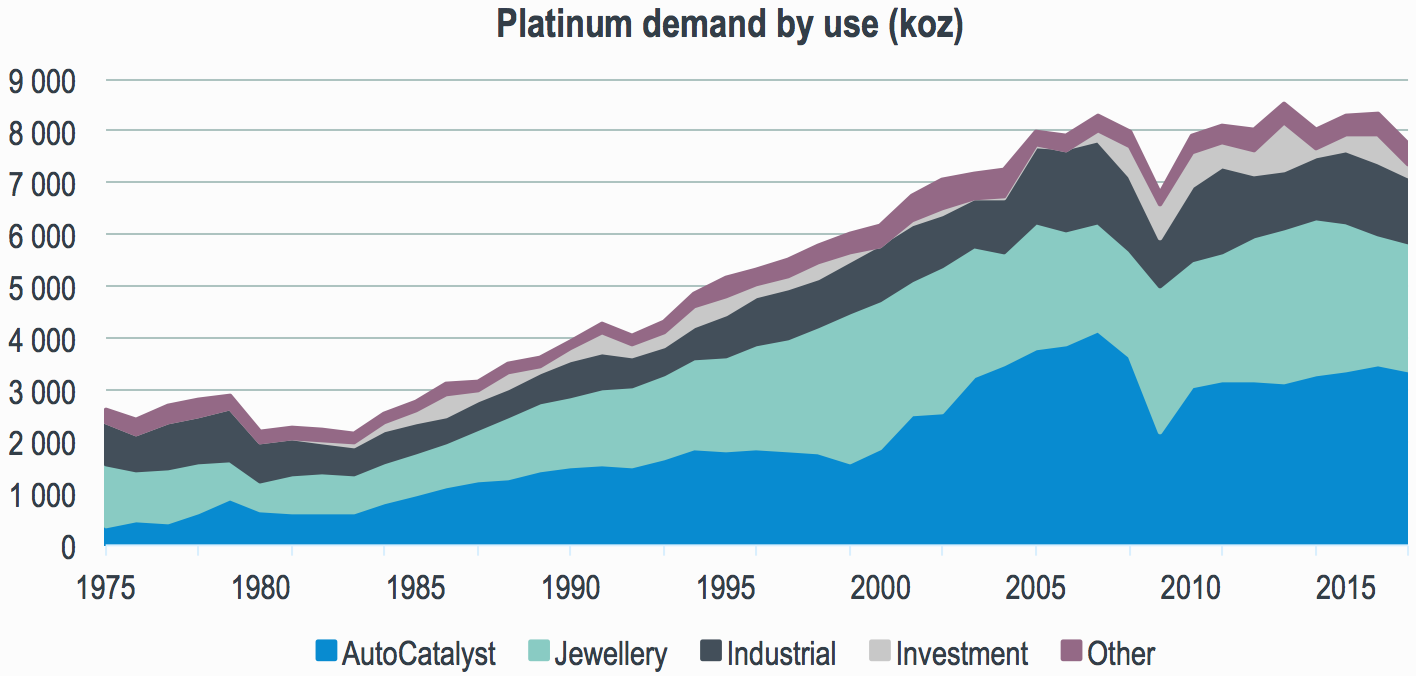

To provide some context, platinum has three main uses: jewellery (30%), as a catalyst in various industrial applications (20%) and as a catalyst in gasoline vehicles (40%). The role of platinum in gasoline vehicles (predominantly diesel) is to facilitate the chemical process of oxidising dangerous carbon monoxide into carbon dioxide and water vapour. Increased emission standards in the preceding decades have led to increased demand for platinum as an autocatalyst. However, the global financial crisis, more efficient use of the metal and the recent dislike and distrust of diesel in Europe has led to demand coming under pressure over the past decade, as the blue bar in the graph shows:

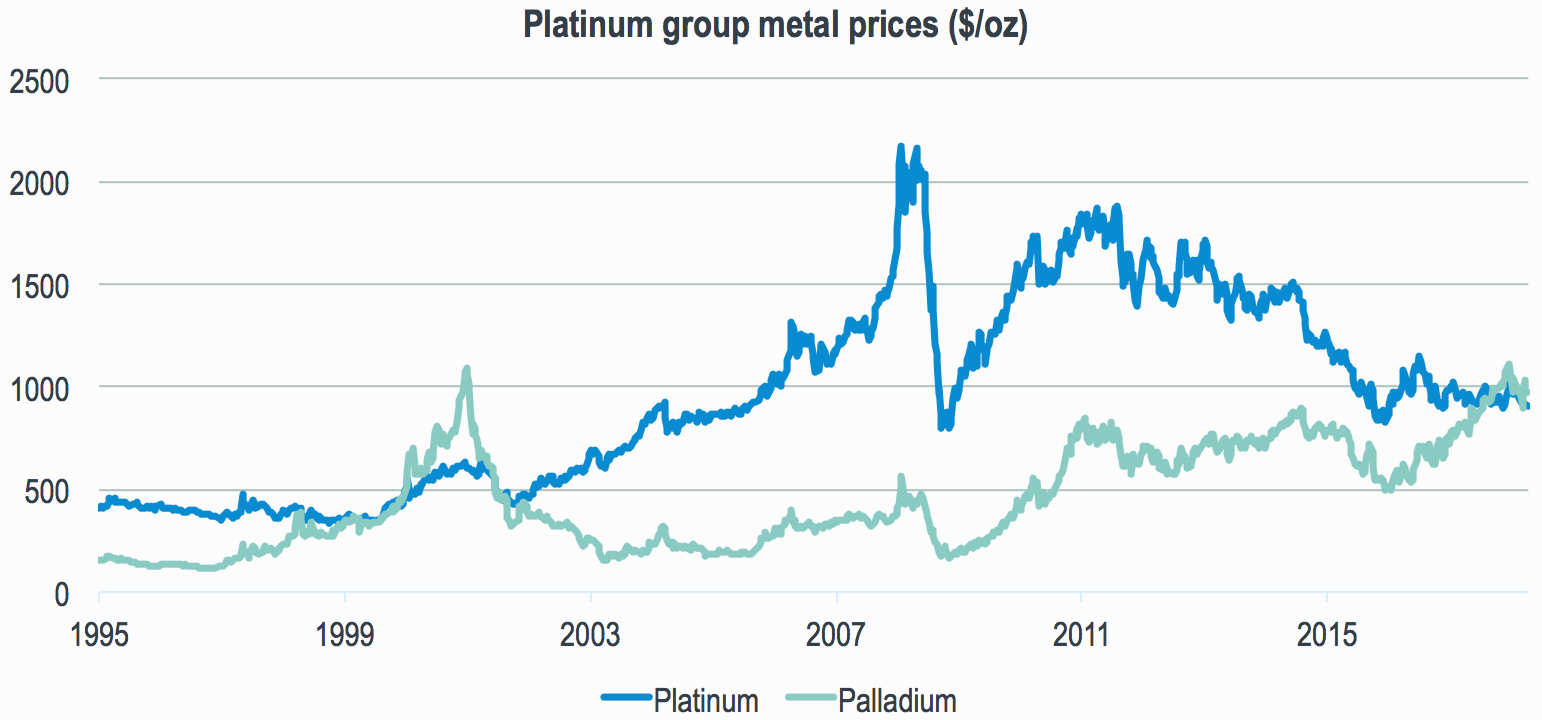

The decline in the demand for diesel, specifically in Western Europe, has resulted in an increase in the sales of petrol vehicles, which in that region predominantly use palladium (in petrol vehicles, platinum and palladium are equally effective). Consequently, the palladium price has increased to historic highs, rising above the platinum price for only the second time in history.

Although an increasing palladium price is positive for South African PGM producers, for most, the bulk of their PGM production is platinum. For example, Impala produces around 50% platinum, 30% palladium and 20% other PGMs, making the platinum price its most important variable. In the medium term, palladium autocatalysts may be switched to platinum in gasoline vehicles, which would imply that the palladium and platinum price should trade in close proximity to one another.

This graph shows the price of platinum and palladium over time:

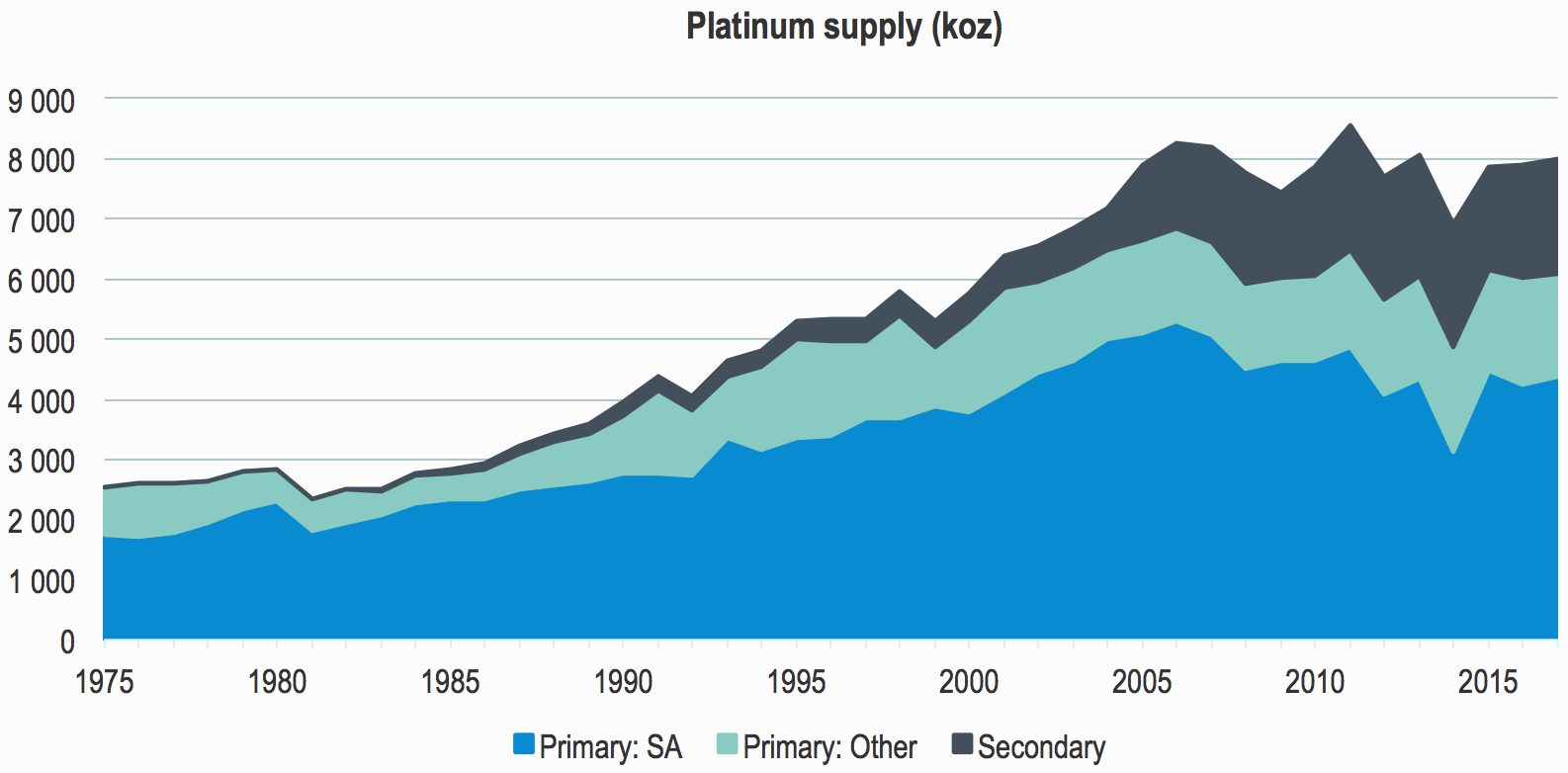

Around 70% of the world’s primary platinum supply comes from South Africa – ±4 200 kilo ounces (koz) per annum. Most of the mines are deep underground and labour intensive, with costs growing at above-inflation rate. At current PGM prices, more than half the industry is unprofitable. The status quo is not sustainable, and unprofitable supply needs to exit the market in order to set the balance right.

Lonmin, which represents about 700koz per annum of platinum supply, is on the brink of bankruptcy. Were it not for an all-share offer by Sibanye Stillwater late in December, the company would default on its debt. However, even though the entire 700 koz is not exiting the market, old shafts producing around 200–300koz are closing during the next couple of years, irrespective of bankruptcy.

Primary supply from South Africa has decreased by almost 1 000koz over the past decade. Unfortunately, this has been offset by an increase in recycled supply. Platinum is a very recyclable metal, which implies that more ounces need to exit the market if demand doesn’t respond. Based on past data, the rate at which recycled material enters the market appears to have normalised, which suggests that the incremental disruption of secondary supply is likely to be less going forward.

This graph shows a breakdown of platinum supply by source:

Impala Platinum is priced to be the next Lonmin, but we don’t believe this assessment is correct. The company can weather a further downturn, should it occur. Impala’s balance sheet carries little net debt, which was recently refinanced with a 2022 maturity. In addition, the company has further debt facilities in place until at least 2021.

Impala isn’t the weakest link in the industry, so a further downturn will likely lead to other producers removing supply from the industry first, which will have a positive impact on PGM pricing. Also, Impala is positioning itself to operate in a low PGM-price environment by closing unprofitable shafts over time and focusing on lower-cost growth shafts. The next couple of years will be uncomfortable, however, with further worker lay-offs and cost-cutting measures required.

In conclusion, we’re not overly optimistic about the South African platinum industry in the long term, but we believe the doom-and-gloom scenario, which the market is largely pricing in, is the less likely outcome. In our view, Impala Platinum is doing the necessary restructuring in order to survive even in a low PGM-price environment, with debt unlikely to be a problem in the next three years. We believe the investment case still makes sense, but patience is required to see it unfold.

We constantly challenge the norm. Our investment process is a thorough and diligent one.

Michael York has spent 21 years in Investment Management.

Have a question for Michael?