Stay abreast of COVID-19 information and developments here

Provided by the South African National Department of Health

SA equities:

is it different this time?

The poor performance of equities – the South African market in particular – in recent weeks has left punch-drunk investors questioning the wisdom of remaining in shares. We’ve always argued that despite short-term market drama, traditional financial laws will hold sway over the long term – and that the five most dangerous words in investments are ‘this time it’s different’. Are we perhaps being naïve in not recognising that maybe this time, the market slump is different? The barrage of negative news we’re faced with on a daily basis in our country is, after all, hard to ignore – and foreign investors are certainly taking note.

In April, we held the view that provided our clients’ equity exposure is aligned with their investment requirements and risk profile, they should stay the course with this asset class – both locally and globally. We argued that if tried-and-tested financial laws continue to hold, patient investors will be justly rewarded through investment cycles for the extra risk taken in investing in equities. We also said the valuation of South African equities in particular wasn’t unreasonable, and it would therefore not make sense to sell assets that are no longer expensive.

South African shares have come under severe pressure in recent weeks, however, and disillusioned investors are increasingly looking to lower-risk asset classes to protect their capital. And it’s not only local equities that have slumped – US-listed shares that were the star performers on the international equity stage have also retreated from recent highs. The question is: were our earlier views naïve? Are shares still a wise choice under the circumstances?

We warned in April that sceptics would certainly argue that ‘normal’ financial laws may no longer be valid – that this time, it is different – for these reasons:

While there are clearly legitimate reasons for the dismal returns of equity markets of late, it should be remembered that when investors start to question a particular asset class, emotion – especially fear – is never far from the surface. And when jittery investors start overreacting and making decisions based on recent short-term experience, it’s usually at precisely the wrong time.

In a bull market, analysts love to quote one of legendary investor Warren Buffett’s golden rules of successful long-term investing: ‘Attempt to be fearful when others are greedy, and greedy only when others are fearful.’ The problem is it’s extremely tough to apply this rule in the face of overwhelmingly negative news flow and market reaction to it. As hedge fund manager Mark Sellers puts it: ‘Everyone thinks they can do this, but when the market is crashing, almost no one has the stomach to buy. When the market is going up almost every day, you can’t bring yourself to sell.’ In the current environment, the fear in the financial markets is palpable.

When we at Sanlam Private Wealth consider our investment strategy for clients’ money, we look only at the facts, not fads. We unemotionally consider price, focus our research effort on establishing the correct perspective, and rely on the evidence of historic price patterns to design a rational strategy that will best serve our clients’ long-term investment needs. In this process, we assess the relative attractiveness of all asset classes, both local and global.

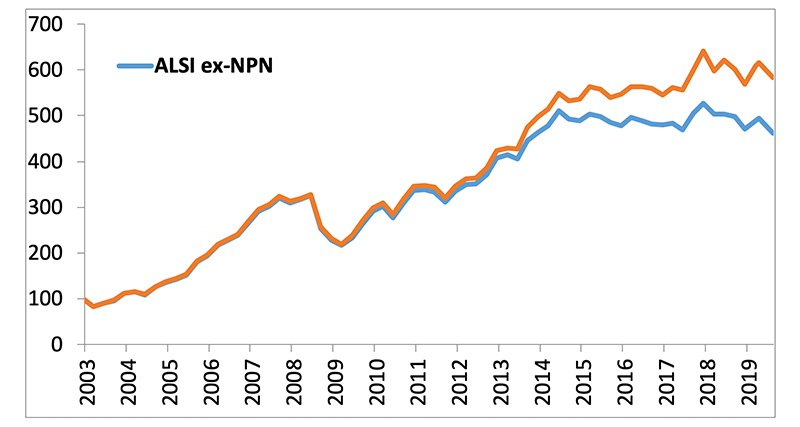

At the moment, it’s clear that the proverbial elephant in the room is the exposure our clients have to equities, particularly South African equities. There can be no doubt that the poor performance of shares in recent years has contributed significantly to the notion that ‘this time, it’s different’ for this asset class. The performance of local equities, excluding Naspers (blue line), versus that of the overall global equity market (orange line) can be seen on the chart below:

Global and local (ex-NPN) equity prices

Source: Bloomberg, SPW research

This chart clearly illustrates that:

In investment speak, one could argue that if you remove Naspers from the picture, local equities have in fact been in a bear market – and in our experience, investors don’t act rationally in bear markets. Normal investment principles, such as consideration for the value of an asset, play second fiddle to the narrative of the day. Indeed, this narrative is being extrapolated into perpetuity – investors see a low probability that the current tough circumstances will ease up any time soon and that the investment environment will revert back to what might be considered ‘normal’.

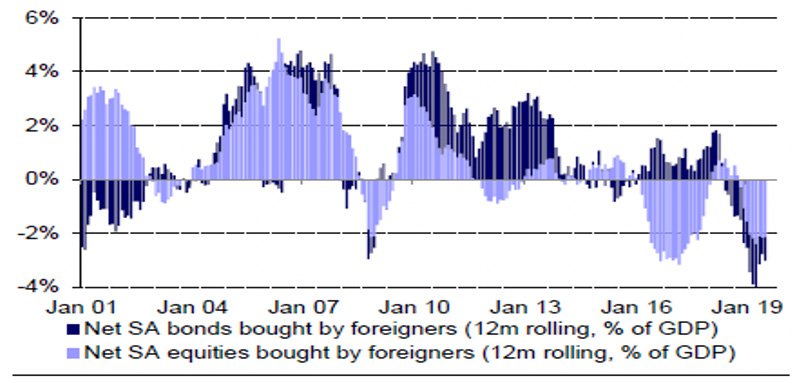

In response, investors have voted with their money. Given the policy uncertainty, fiscal risks and pedestrian economic growth in South Africa, foreign investors have been net sellers of local equities since 2016, and this trend has accelerated over the past few months as the macro news flow has deteriorated. In fact, foreign investors have also been selling off local bonds. In all, we’ve witnessed the biggest net sale of South African assets since the dark days of 2001.

The data certainly suggest that foreigners are acting in a fearful manner, as the chart below shows:

Foreign purchases/sales of SA equities and bonds

Source: FTSE/JSE, Credit Suisse research

So where does this leave South African investors? We still maintain that despite short-term setbacks, over the long term, price, perspective and pattern will continue to drive future performance. In our view, long-term investment principles, which have held sway for decades, will continue to apply despite all the short-term drama – there’s no reason why they should now suddenly be invalid. The notion of ‘buying when others are fearful’ is therefore not a naïve approach.

We’re not for a moment suggesting that we should ignore the current perspective of extreme uncertainty on both the local and global fronts – we should therefore continue to manage the asset allocation of portfolios actively. Investors should recognise, however, that markets are dynamic, and tend to price in concerns (which of course provides longer-term opportunities). In the current environment, markets have already responded to the poor outlook:

The bottom line is that we at Sanlam Private Wealth have not changed our long-term views on South African equity markets. We believe that investors who want to grow their wealth in real terms – over time – shouldn’t be too hasty in exiting this asset class. It’s likely that local share prices may decline even further over the short term. However, it’s important to remember that over the long term – and by this we mean at least 10 years – equities have consistently and significantly outperformed every other asset class. Of course, each investor’s proportionate exposure to equities needs to align with their unique risk profile and investment requirements.

We’re by no means arguing that investors should have unrealistic return expectations for equities. We can’t ignore the fact that the global economic cycle is mature, and we can’t expect our market to disengage from global trends. However, other asset classes are currently even less appealing from a long-term perspective. We struggle to understand why rational long-term investors would buy a 10-year German government bond and accept a guaranteed negative return of 0.4% if held until maturity. It simply doesn’t make sense when investors have the opportunity to instead buy a quality global share with a free cash flow yield in excess of 6% and with realistic company prospects of compounding earnings in the future.

In the final analysis, we don’t think it’s different this time. Yes, investors are now facing increased risks, both locally and globally, and there are of course no guarantees when it comes to investing. However, periodically increased risk isn’t uncommon within the broader context of traditional long-term investment cycles. The secret is to reduce risk in investment portfolios in good times, and then gradually increase risk during bad times – when the price is right. The increased risk in portfolios will then reward investors when – not if – the cycle improves.

Using your equity portfolio to secure credit allows you fast access to capital.

Sizwe Mkhwanazi has spent 14 years in Investment Management.

Have a question for Sizwe?